Does Majority Voting Improve Board Accountability?

Directors have traditionally been elected by a plurality of the votes cast. This means that in uncontested elections, a candidate who receives even a single vote is elected. Proponents of shareholder democracy have advocated a shift to a majority voting rule, in which a candidate must receive a majority of the votes cast to be elected. Over the past decade, they have been successful, and the shift to majority voting has been one of the most popular and successful governance reforms.

Yet critics are skeptical as to whether majority voting improves board accountability. Tellingly, directors of companies with majority voting rarely fail to receive majority approval—even more rarely than directors of companies with plurality voting. Even when such directors fail to receive majority approval, they are unlikely to be forced to leave the board. This poses a puzzle: Why do firms switch to majority voting, and what effect, if any, does the switch have on director behavior?

We empirically examine the adoption and impact of a majority voting rule using a sample of uncontested director elections from 2007 to 2013. We test and find partial support for four hypotheses that could explain why directors of majority voting firms so rarely fail to receive majority support: selection, deterrence or accountability, electioneering by firms, and restraint by shareholders.

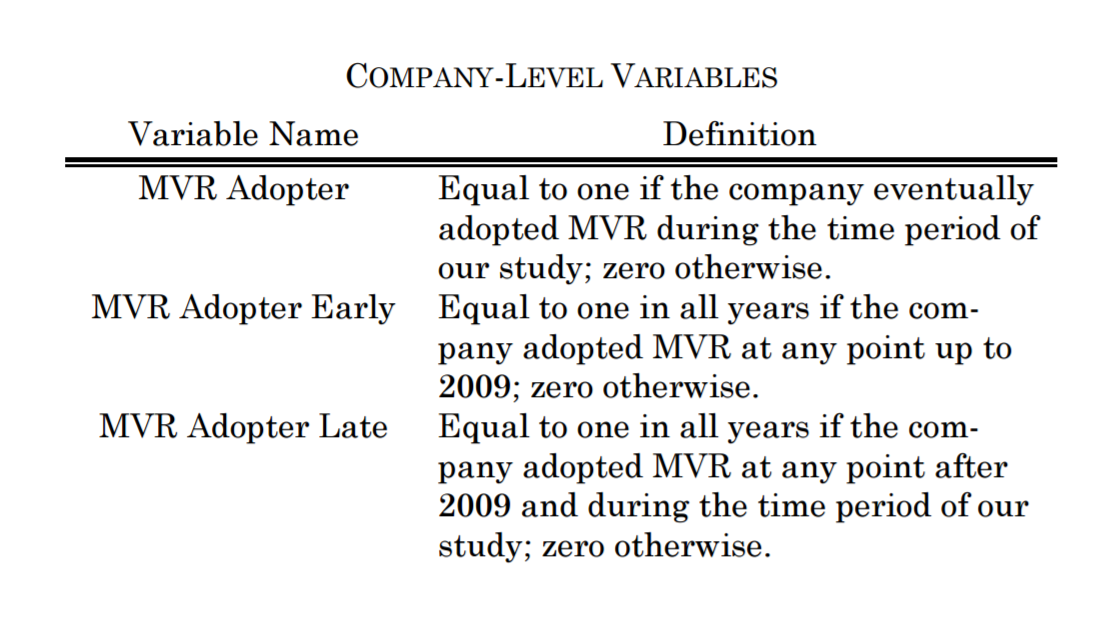

Our results further suggest that the reasons for and effects of adopting majority voting may differ between early and late adopters. We find that early adopters of majority voting were more shareholder responsive than other firms, even before they adopted majority voting. These firms seem to have adopted majority voting voluntarily, and the adoption of majority voting has made little difference in their responsiveness to shareholders going forward. By contrast, for late adopters we find no evidence that they were more shareholder responsive than other firms before they adopted majority voting, but we find strong evidence that they became more responsive after adopting majority voting.

Differences between early and late adopters can have important implications for understanding the spread of corporate governance reforms and evaluating their effects on firms. Rather than targeting the firms that, by their measures, are most in need of reform, reform advocates instead seem to have targeted the firms that were already the most responsive. These advocates may then have used the widespread adoption of majority voting to create pressure on the nonadopting firms to conform. Empirical studies of the effects of governance changes thus need to be sensitive to the possibility that early adopters and late adopters of reforms differ from each other and that the reforms may have different effects on these two groups of firms.

I. The Shift from Plurality to Majority Voting

Traditionally, directors in most companies were elected by a plurality of the votes cast.19 This plurality standard was (and remains) the default rule in Delaware and most other states.20 A problem with the traditional plurality standard is that it has little meaning in an uncontested election, which most board elections are.21 If the number of nominees to the board is equal to the number of board seats to be filled, every nominee who receives at least one vote will be elected. As a result, even a nominee who has minimal support among shareholders is assured of getting on the board.22 Similarly, in the absence of a competing nominee, disgruntled shareholders cannot unseat a director by failing to vote in favor of his or her election.23

Shareholder inability to cast an effective vote against director candidates has not prevented shareholders from expressing their dissatisfaction with director nominees. In 1993, Professor Joseph Grundfest published an article urging investors to engage in symbolic “vote no” campaigns to express concerns about an issuer’s performance.24 Institutional investors began to engage in “withhold”-vote campaigns.25 One highly publicized example was the effort led by the California Public Employees’ Retirement System (CalPERS) to “withhold” votes at Disney from director nominee Michael Eisner.26 The effort was enhanced by the growing influence of proxy advisory firms such as ISS,27 which offer institutional investors recommendations on which director nominees to target with “withhold” votes.28

Beginning in 2005, shareholder activists began to push for changes in the voting standard.29 Initially, some issuers adopted a director-resignation policy—a board policy requiring each board nominee to submit a conditional offer to resign if he or she does not receive a majority of the votes cast at the next election.30 Later on, issuers amended their bylaws or charters to adopt a majority standard for uncontested director elections. Under the strict majority standard, a nominee is elected only if he or she receives more “for” votes than “against” votes.31

Even under a strict majority standard, in which a nominee is not elected if he or she does not get a majority of “for” votes, a failure to be elected does not automatically mean that the nominee will be removed from the board.32 Under the laws of Delaware and many other states, an incumbent director continues as a holdover director until the director resigns, the director is removed, or a successor is elected.33 Thus, even if an incumbent director fails to secure a majority of “for” votes, the director often stays in office, at least for the time being. In addition, statutes generally provide, at least as a default matter, that the board of directors has the authority to fill vacancies on the board.34 As a legal matter, nothing prevents the board from appointing the very person who failed to receive a majority of “for” votes to fill the vacancy.

MVRs have been embraced by both investors and issuers.35 As a result, the movement from plurality to majority voting has been relatively rapid, especially at large companies. Some type of MVR was used by approximately 16 percent of S&P 500 companies in February 2006.36 As of January 2014, approximately 90 percent of S&P 500 companies used some form of majority voting.37 The shift to majority voting at smaller companies has been less pronounced. As of 2012, 52 percent of mid-cap companies had adopted majority voting.38 The percentage of small-cap companies with majority voting as of 2012 was far lower—only 19 percent.39

Many commentators have argued that majority voting enhances director accountability to shareholders. In 2005, then–ISS Vice President Stephen Deane wrote that majority voting “holds the potential to enable a new era in constructive dialogue between corporations and their owners.”40 The Council of Institutional Investors supported the adoption of majority voting and urged the NYSE and NASDAQ to impose a majority voting requirement as a listing standard.41 Professor Lucian Bebchuk wrote that “given the clear and widely accepted flaws of plurality voting, majority voting should be the default arrangement.”42 Professor Lisa Fairfax argued that “[t]o the extent the threat of losing a board seat impacts board behavior, majority voting increases shareholders’ ability to influence board behavior.”43

Few studies have examined the effect of majority voting empirically. An early study by Professors William Sjostrom and Young Sang Kim looked at stock price reactions to firms’ adoptions of majority voting and found no statistically significant market reactions.44 The study suggested that the lack of impact was due, in part, to the fact that majority voting does not in fact “give[ ] shareholders veto power over incumbent directors.”45 Rather, the authors concluded, MVRs were “smoke and mirrors” because the board ultimately had the power to retain a losing director.46

Professors Jie Cai, Jacqueline Garner, and Ralph Walkling looked at 481 firms that adopted majority voting from 2004 to 2007.47 Their study found that early adopters initially experienced positive abnormal returns in response to the adoption announcement.48 The study found that, over a one-year time period, however, the “adoption of majority voting has little effect on director votes, director turnover, or improvement of firm performance.”49 Importantly, although poorly performing firms were more likely to adopt an MVR, their performance continued to deteriorate after the adoption of majority voting.50 The authors therefore concluded that majority voting was a “paper tiger.”51

Finally, Professors Yonca Ertimur, Fabrizio Ferri, and David Oesch looked at shareholder proposals on majority voting.52 Using a regression-discontinuity design, they showed that the adoption of these proposals is associated with a positive abnormal stock price return.53 Moreover, using a matched sample (based on propensity scores), they found that firms that have adopted majority voting are more likely to implement shareholder proposals54 and less likely to experience high levels of “withhold” votes for directors in consecutive annual meetings.55

This Article contributes to this literature by distinguishing among, and empirically examining, several possible explanations for the differential voting patterns observed between firms that employ plurality voting and those that employ majority voting. Moreover, this Article is the first to differentiate early adopters of majority voting from late adopters and to present evidence that factors explaining the voting patterns differ significantly for these two sets of firms.

II. Possible Explanations for the Different Voting Patterns

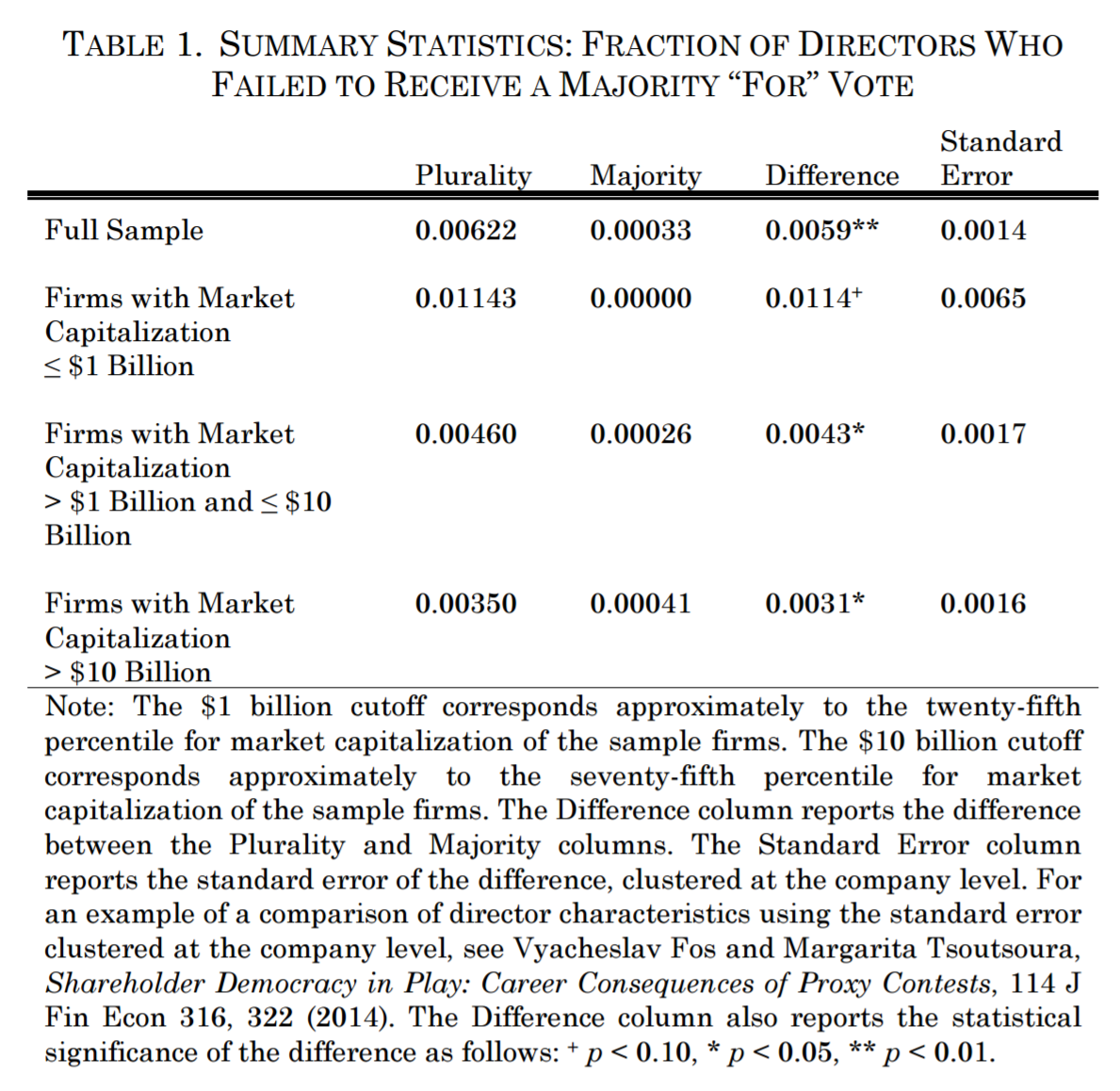

Elections governed by an MVR exhibit a strikingly different vote pattern from elections governed by a PVR. As noted above, directors elected under an MVR are far more likely to receive a majority “for” vote. In our sample, which consists of almost sixty-five thousand uncontested director elections at S&P 1500 companies between 2007 and 2013, only 0.033 percent of director nominees in elections governed by an MVR failed to receive a majority of votes cast. By contrast, in elections governed by a PVR, 0.622 percent of candidates failed to garner a majority. The difference is statistically significant at the 1 percent level.

Table 1 reports summary statistics on the fraction of directors that failed to receive a majority “for” vote. We also report the summary statistics for subsets of our sample divided according to market capitalization.

Several hypotheses may account for the difference in voting patterns between MVR and PVR firms. Companies that adopt majority voting may simply be different from companies that do not. This is a standard selection effect—“good” companies self-select into adopting majority voting.56 Ex post, nominees at these companies are less likely to receive a high “withhold” vote, but this effect is not caused by majority voting but rather by the underlying good-governance factors that led the company to adopt majority voting. We refer to this explanation as the selection hypothesis.

Alternatively, the different voting patterns may be caused by the difference in voting rules. We refer to this explanation as the causation hypothesis. In particular, there are three different ways in which the voting rules may cause differential voting patterns, each with different normative implications. The first possibility, that an MVR increases director accountability by making directors more responsive to shareholder interests, is what has driven investors to support the implementation of majority voting.57 We refer to this form of the causation hypothesis as the deterrence (or accountability) hypothesis. Notably, confirming the deterrence hypothesis does not necessarily demonstrate that directors who are subject to majority voting are making better decisions. Catering to shareholders may not lead to increased firm value.58 Indeed, skeptics might describe the deterrence effect as making directors more responsive to ISS, given the reputed influence of ISS over shareholder voting decisions.59 To avoid the implication that an MVR induces superior decisions, we use the term “shareholder friendly” or “shareholder responsive” governance to refer to actions that have a lower likelihood of inducing “withhold” votes.

A second possibility is that companies that have adopted majority voting may engage in more campaigning in close elections because the implications of receiving a majority “withhold” vote are more severe. Relatedly, these companies may lobby ISS harder not to issue a “withhold” recommendation. We refer to this form of the causation hypothesis as the electioneering hypothesis.

ISS has a practice of notifying S&P 500 companies that it intends to issue a “withhold” recommendation and offering them a forty-eight-hour window during which they can engage with ISS about the recommendation.60 It is commonplace for issuers to engage with ISS, both during this window and otherwise, in an attempt to influence ISS’s recommendations.61 Upon receiving such a warning, MVR companies may make greater efforts to persuade ISS not to issue that recommendation than PVR companies do. Because a positive ISS recommendation virtually guarantees that the election will not be close,62 persuading ISS not to issue a negative recommendation is an effective strategy to guarantee a majority “for” vote.

In addition to lobbying ISS, companies can address shareholders directly. Companies can communicate individually with larger institutional investors to explain why a nominee should be elected and the value of the nominee to the company. They might also hint that the company would not look favorably on any institution that votes against the nominee or that the company would be less inclined to answer questions by investment professionals who work for such an institution. Companies can also communicate publicly with shareholders through formal proxy solicitation materials. Companies can engage the services of a proxy solicitation firm to communicate with shareholders, and can increase the efforts exerted by such a firm in the case of a close election. All these solicitation efforts entail costs, but when the consequences of failing to get a majority of “for” votes are more severe, as they are under an MVR, companies may be more willing to incur these costs.

Notably, companies know when an election is likely to be close. Indeed, they have detailed information about the preliminary voting tallies well before the shareholders meeting. Historically, Broadridge Financial Solutions, the firm that runs the mechanics of proxy solicitation and vote tabulation,63 has provided interim voting information to issuers from the date that the proxy materials are distributed to investors up through the date of the shareholders meeting.64 This information enables companies to predict the outcome of the vote and to shape their shareholder-engagement policies accordingly.65

Finally, shareholders may be more reluctant to cast a vote against a nominee when a failure to get a majority of “for” votes could result in the ouster of the nominee. Shareholders may view casting a “withhold” vote under a PVR as a symbolic protest vote. Indeed, when Professor Grundfest first popularized “vote no” campaigns as a way to deal with legal developments that reduced the effectiveness of the market for corporate control as a form of discipline, he explicitly extolled the value of such campaigns as a symbolic gesture rather than a tool with a meaningful potential for changing board composition.66 In contrast, shareholders may be concerned that a failure to elect a full slate of directors at a company with an MVR may interfere with board functioning and therefore may be reluctant to cast “no” votes. Similarly, Professors Cai, Garner, and Walkling suggest that institutional investors may fear that such a failure would adversely affect stock price and, as a result, may be more reluctant to vote against a director in a majority voting firm.67 We refer to this form of the causation hypothesis as the shareholder-restraint hypothesis.

In an earlier article, two of us analyzed the consequences of majority “withhold” votes at companies using a PVR.68 In examining Russell 3000 companies in the 2008 and 2009 proxy seasons, we found that only 3 of 112 director nominees who failed to receive a majority vote under a PVR left the board, at least immediately—a much lower percentage than our results here for nominees at companies using an MVR.69 However, for about two-thirds of the other nominees, the company and the director took steps that effectively addressed the underlying reason for the high “withhold” vote.70 We concluded that “withhold” votes at companies with plurality voting were effective in inducing companies and directors to change their behavior (though not in inducing a change in board composition).

Moreover, because most shareholders seem satisfied if companies and directors change their behavior—as judged by the low percentage of “withhold” votes received in subsequent elections by nominees who took corrective measures but remained on the board—we conjectured that the main aim of “withhold” votes at these companies was to induce changes in behavior and not necessarily to oust nominees from their board seats.71 For a shareholder who wants to induce a change in behavior but not a turnover in board composition, the voting decision under a plurality regime is an easy one. The voting decision under an MVR is more complicated. If a director or nominee faces a real risk of not receiving a majority of “for” votes, a decision to vote “against” may overshoot by inducing the director to leave the board. Under a majority regime, such a shareholder may therefore decide to cast a “for” vote (or abstain from voting) when, under a plurality regime, the shareholder would have voted against a nominee.

The four explanations we have discussed—the selection, deterrence or accountability, electioneering, and shareholder-restraint hypotheses—are not mutually exclusive. Each explanation may contribute to some extent to the difference in voting patterns. Moreover, different explanations may apply to different groups of firms. As noted above, majority voting has swept through the largest firms and has become increasingly common in smaller publicly traded companies. It is possible that majority voting, and perhaps corporate governance reforms more generally, will be adopted first by firms that are already very responsive to shareholders and thus can adopt the reform at very low cost—a selection effect. At some point, however, a reform may become accepted as a best practice, and later adopters may feel compelled to adopt the reform and become more responsive as a result—a causal effect. It is thus plausible that companies with shareholder-friendly governance adopted majority voting relatively early, but that companies that adopted majority voting later on do not differ much from nonadopters. Alternatively, it may also be plausible that reform advocates first pressured those companies with the least shareholder-friendly governance—those most in need of governance changes—to adopt majority voting.72 In the next Part, we describe various tests directed at examining the importance of each of these explanations for the sample as a whole and for different subsets of companies.

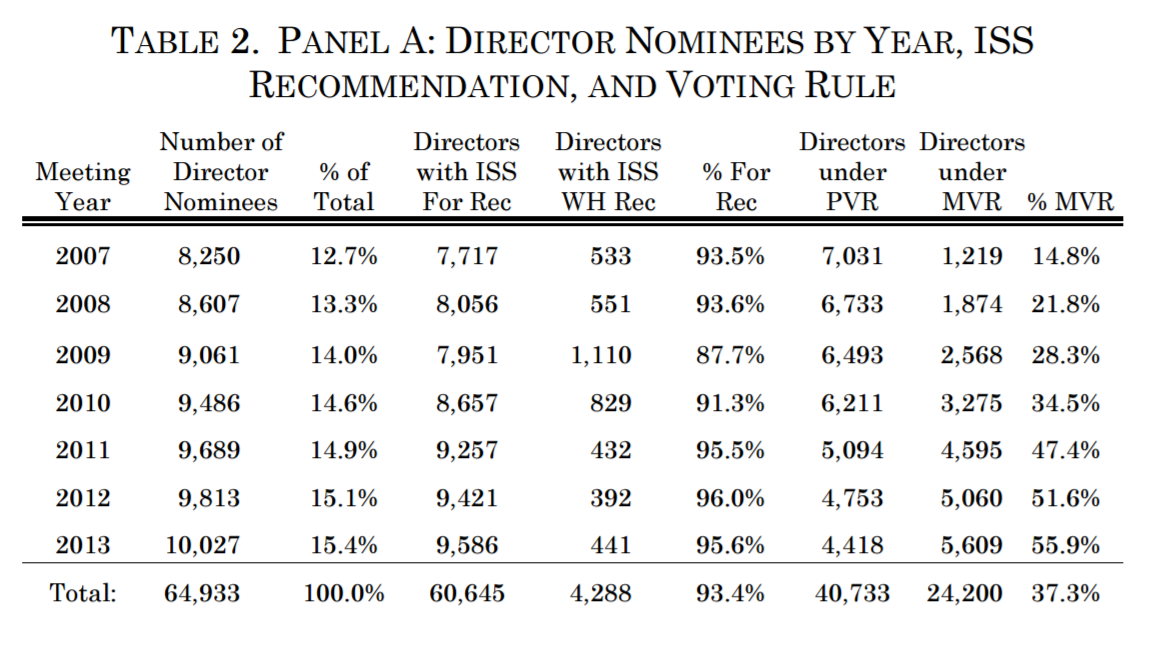

We collected data on shareholder voting in director elections at S&P 1500 companies for the years 2007 through 2013. Our data set consists of 64,933 elections, with about 9,000 observations per year. We obtained voting data on director elections at S&P 1500 companies from ISS. We started with 65,751 observations of uncontested director elections in the data set. We dropped those observations in which the vote requirement was either unknown or not majority or plurality voting for the election of directors, leaving 65,690 observations. We then dropped observations involving entities other than corporations (such as real estate investment trusts), leaving 64,933 observations.

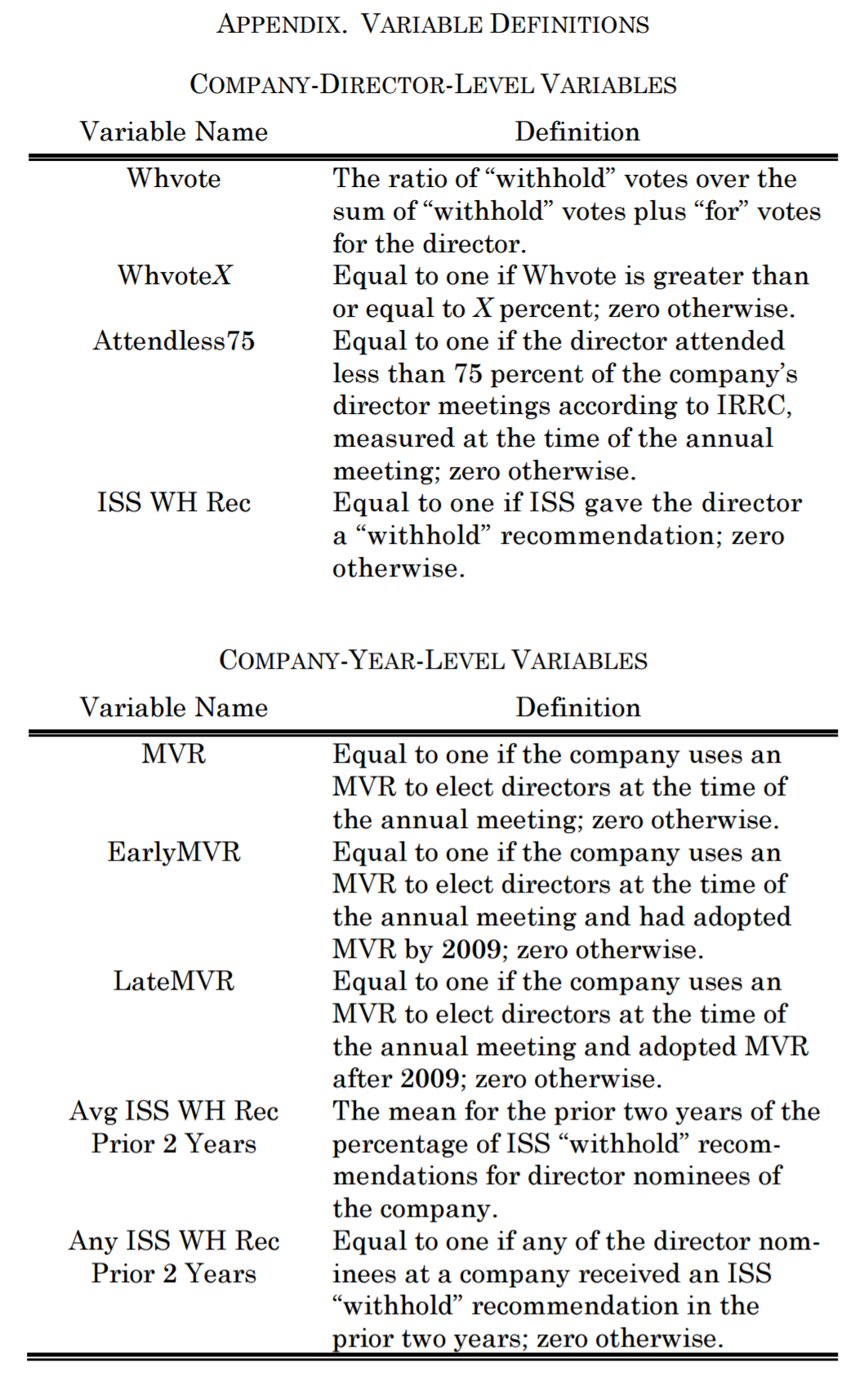

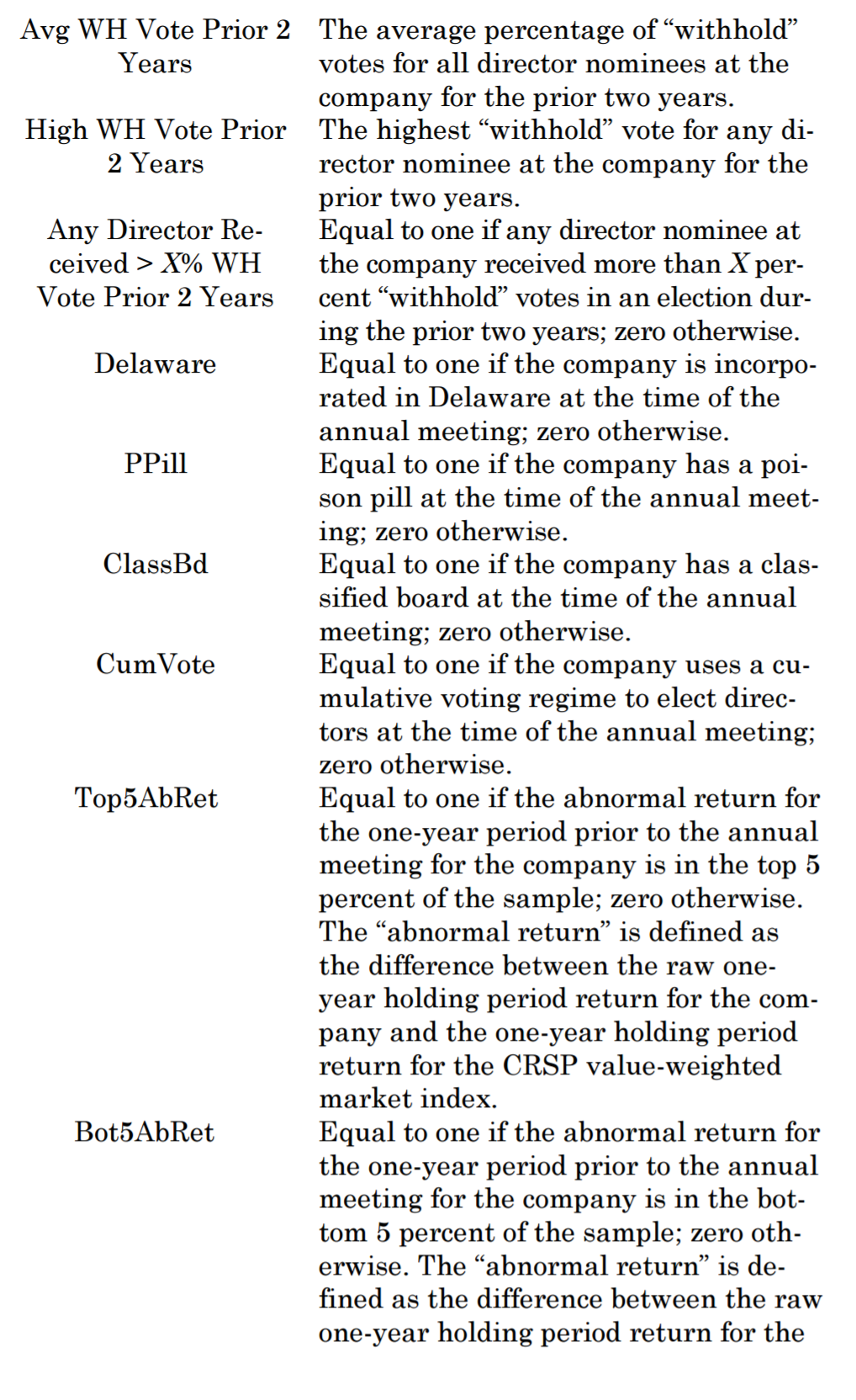

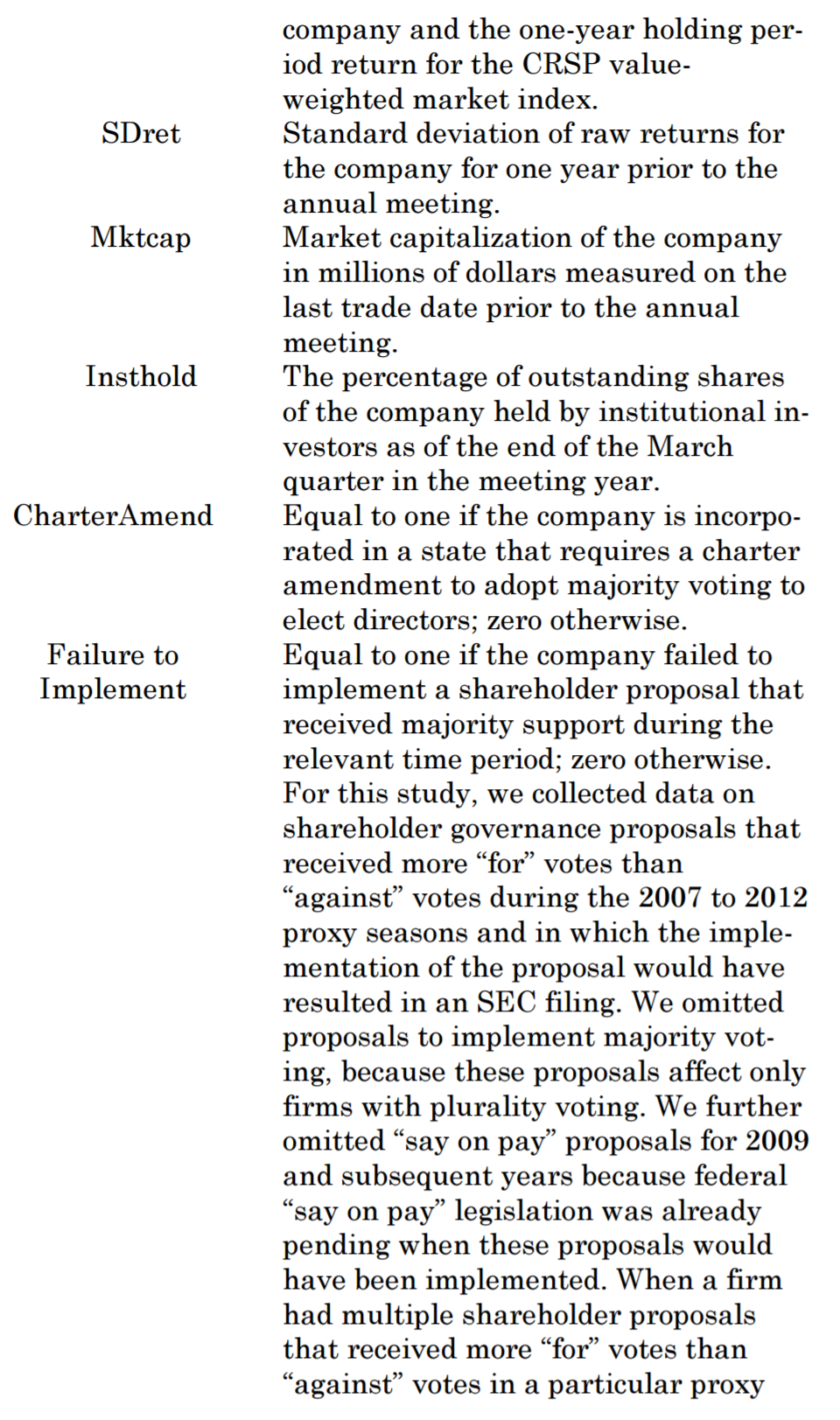

Our data include the votes cast “for” and “withhold” (or “against”)73 on each nominee, whether the election was governed by an MVR or a PVR, and the recommendation issued by ISS. We also collected information on several director and company characteristics that our past research has identified as associated with the vote outcome.74 We obtained executive compensation data from ExecuComp, stock return data from the Center for Research in Security Prices (CRSP), board composition and director biography data from RiskMetrics Group, institutional investor holdings data from Thomson Reuters, restatement data from Audit Analytics, issue-proposal outcome data from Georgeson, and state-of-incorporation data from Compustat. We also collected certain corporate governance data—including whether the company had an active poison pill, a classified board, or cumulative voting in the year of the election—from RiskMetrics. A description of the variables is in the Appendix.

For the data set as a whole, 37.3 percent of the elections were governed by majority voting, and ISS issued “withhold” recommendations for 6.6 percent of the nominees. The percentage of nominees with ISS “withhold” recommendations (“ISS WH Rec”) peaked in 2009 at 12.3 percent and then declined to 4 percent by 2012, while the percentage of directors subject to majority voting climbed steadily from 14.8 percent in 2007 to 55.9 percent in 2013.75 These results are presented in Panel A of Table 2.76

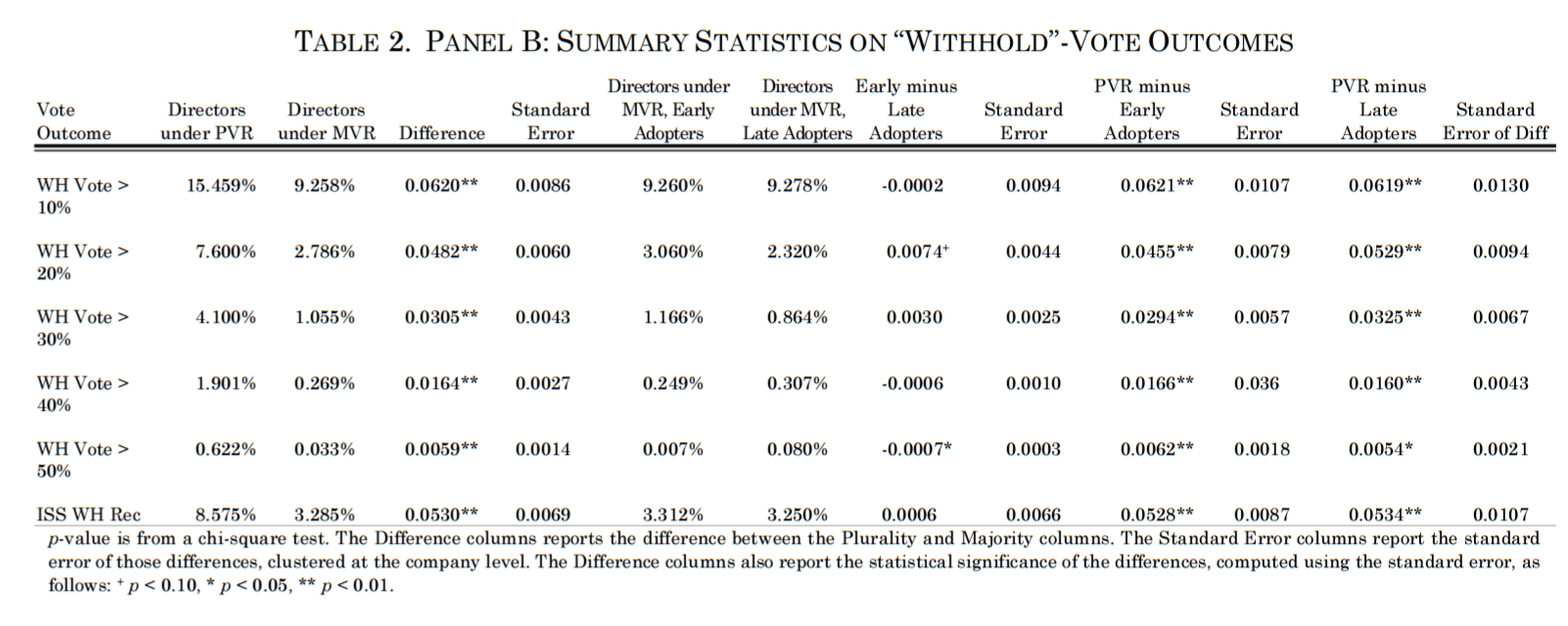

Panel B provides summary statistics on the percentages of directors under a PVR or an MVR that received above specified cutoffs of “withhold” votes. For each cutoff, the difference between the likelihood that directors under a PVR would receive “withhold” votes above the cutoff was higher than the respective likelihood for directors under an MVR and the difference was significant at the 1 percent confidence level. However, the relative frequency gets starker the higher the level of “withhold” votes. For example, the likelihood of getting a majority “withhold” vote is 19 times higher for plurality than for majority vote companies, whereas the likelihood of getting a 10 percent “withhold” vote is only 1.7 times higher. Panel B also provides separate data on companies that had adopted majority voting by 2009 (“early adopters”) and companies that subsequently adopted it (“late adopters”).

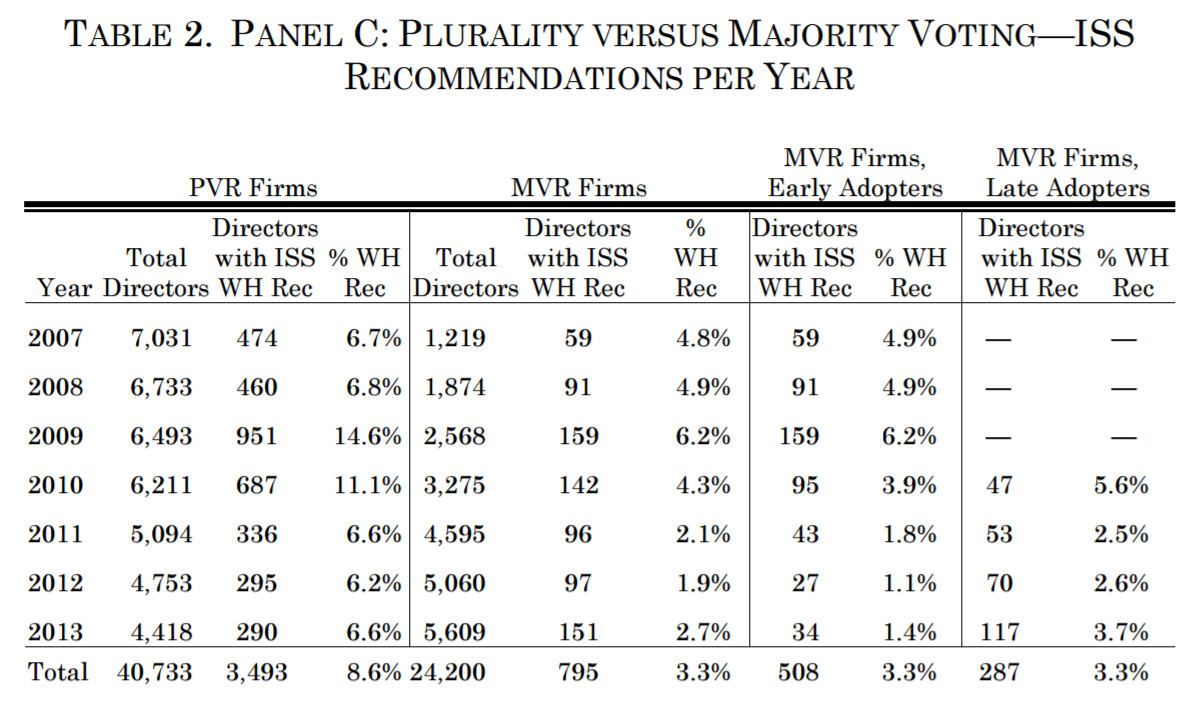

Panel C provides summary statistics on the frequency of ISS “withhold” recommendations. As Panel C shows, nominees subject to an MVR are less likely to receive an ISS “withhold” recommendation than nominees subject to a PVR. The overall frequencies are 3.3 percent and 8.6 percent for majority voting and plurality voting, respectively, a difference that is statistically significant at the 1 percent confidence level.77 Moreover, in each year, the probability of receiving a negative ISS recommendation was lower for nominees subject to majority voting than for nominees subject to plurality voting. The difference between majority and plurality voting regimes is not significant for 2007 and 2008 and is significant at the 1 percent confidence level for 2009 through 2013.78

As noted above, one problem with analyzing the effects of majority voting is that firms that adopt majority voting may be different from firms that do not. Consider, for example, a company that strives to have good corporate governance practices, as judged by ISS, the Council of Institutional Investors, and large mutual funds. As a result, none of its board members (other than the CEO) are employees or have business dealings with the company, its compensation committee employs exemplary procedures, its governance guidelines limit the number of board seats any director may have, and its directors have high attendance rates. Because corporate governance professionals at ISS79 and many institutions80 favor majority voting, the company has also adopted majority voting. For such a company, it is the company’s underlying commitment to shareholder-friendly corporate governance (and presumably the reasons underlying that commitment, such as a committed board and CEO or fear of ISS) that caused both the lower prospect of high “withhold” votes and the adoption of majority voting.

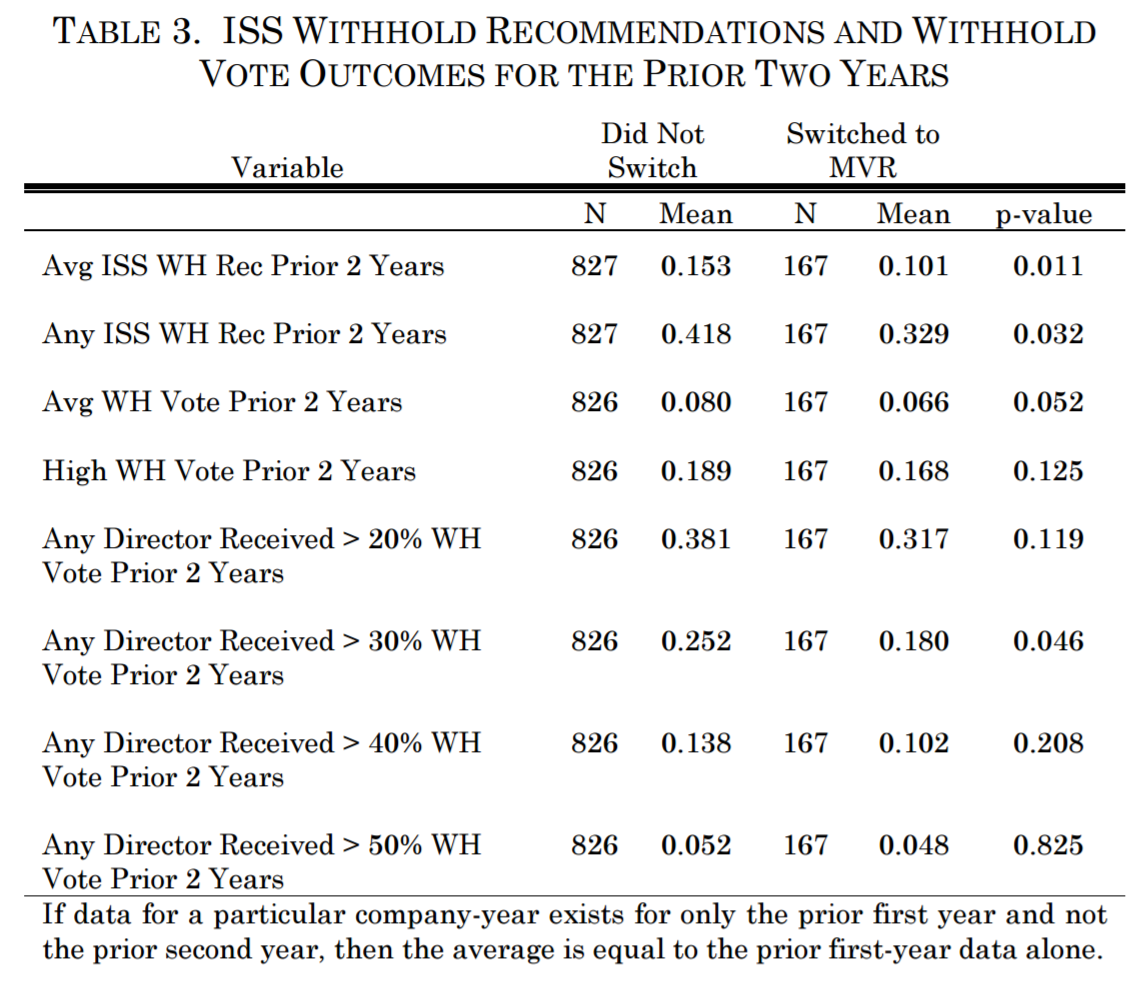

To test for self-selection, we examined whether companies that adopted majority voting are different from those that did not. We compared companies that adopted majority voting in 2011, the year in our data set that saw the largest number of adoptions, with those that retained plurality voting. We then examined various measures of shareholder-friendly governance for the prior two years (2009 and 2010)—including the average percentage of “withhold” recommendations (“Avg ISS WH Rec Prior 2 Years”), whether the company’s nominees had received any “withhold” recommendations (“Any ISS WH Rec Prior 2 Years”), the average percentage of “withhold” votes (“Avg WH Vote Prior 2 Years”), the highest “withhold” vote for any of the company’s nominees (“High WH Vote Prior 2 Years”), and whether any nominee received a “withhold” vote above certain thresholds—both for companies that had switched to majority voting in 2011 and for companies that retained plurality voting in 2011. The results are reported in Table 3.

As Table 3 shows, companies that switched to majority voting in 2011 had a different prior record than companies that retained plurality voting. In the two years prior to the switch, companies that switched in 2011 had a significantly lower percentage of nominees who received a “withhold” recommendation (10.1 percent versus 15.3 percent), a significantly lower likelihood that at least one nominee would receive a “withhold” recommendation (32.9 percent versus 41.8 percent), and a significantly lower likelihood of having a nominee receive a “withhold” vote of at least 30 percent (18.0 percent versus 25.2 percent).

The results reported in Table 3 support the selection hypothesis. They indicate that companies whose nominees receive less ISS support and experience less electoral success are overall less likely to adopt majority voting. To the extent that electoral success in subsequent years is correlated with ISS support and electoral success in prior years, this self-selection would explain at least part of the reason why nominees in companies with majority voting fare better than nominees in companies with plurality voting. We note that our prior research has found a strong association between an ISS “withhold” recommendation and the percentage of “withhold” votes.81

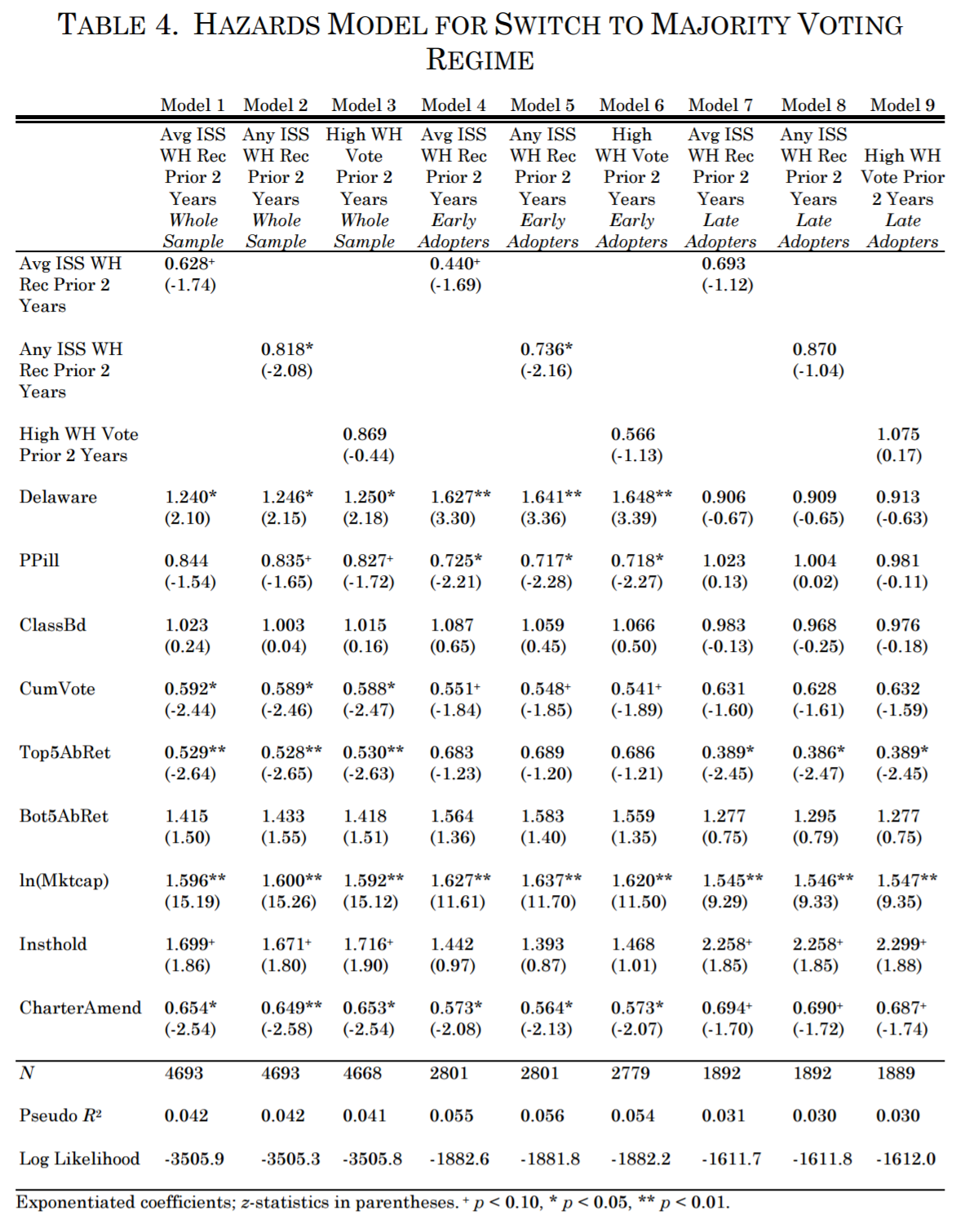

To explore the self-selection hypothesis in greater detail, we estimated a Cox proportional hazards model for the adoption of majority voting during the 2007 to 2012 period. The Cox proportional hazards model is a type of statistical survival model that relates the time to a specified event (in our case, the adoption of majority voting) to various independent variables that may affect the amount of time to the event (such as the fraction of shares that are held by institutional investors). The dependent variable in the Cox proportional hazards model is a switch from a PVR to an MVR. The hazards model initially includes all firms that used plurality voting for the election of directors in 2007. As firms switch to majority voting, they drop out of the regression analysis. The hazards model is consistent with the fact that many firms move from plurality to majority voting, but few if any move back to plurality voting once they have switched to majority voting.

We include as an independent variable in each model either the mean of the percentage of ISS “withhold” recommendations for the prior two years (Avg ISS WH Rec Prior 2 Years); an indicator variable for whether any of the director nominees at a firm received an ISS “withhold” recommendation in the prior two years (Any ISS WH Rec Prior 2 Years); or the highest “withhold” vote for any director nominee at a firm in the prior two years (High WH Vote Prior 2 Years). Also, in all three models we included two additional variables: whether the firm has a standing poison pill (“PPill”) and whether the firm has a classified board (“ClassBd”).82 Because both poison pills and classified boards are frowned upon by governance activists, their presence may indicate that the firm has less shareholder-friendly governance. A finding that firms with a poison pill or with a classified board are less likely to adopt majority voting would thus be consistent with the selection hypothesis.

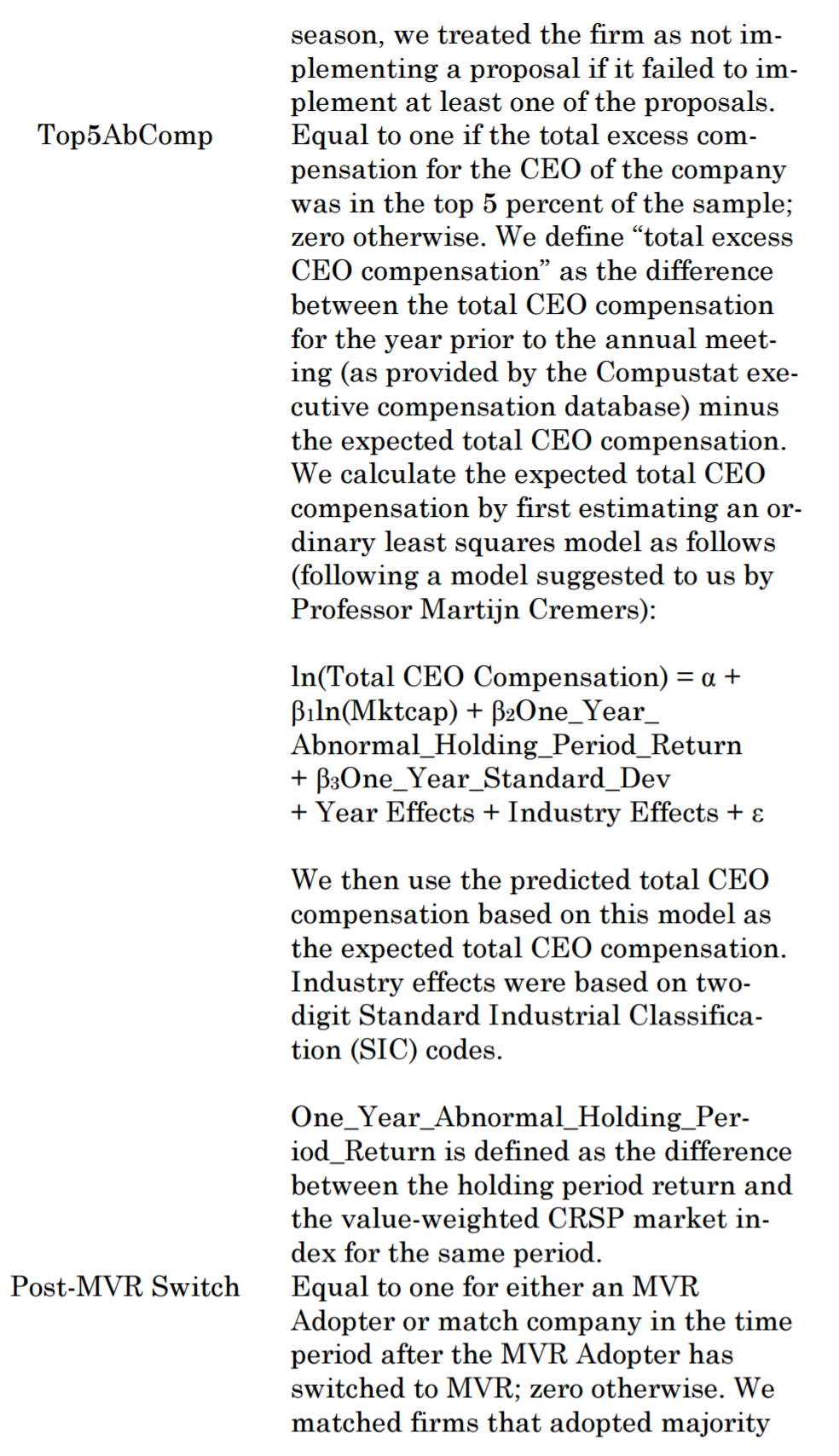

As controls, we included an indicator variable for whether the firm is incorporated in Delaware (“Delaware”); a variable for whether the firm uses cumulative voting (“CumVote”) (the MVR is not well-defined for firms using cumulative voting); two indicator variables for whether the firm was in the top 5 percent or bottom 5 percent of the companies in our sample based on the abnormal return for the one-year period prior to the annual meeting (“Top5AbRet” and “Bot5AbRet”) (firms with better stock performance may be better able to resist pressure to adopt majority voting on the rationale of “never change a winning team”); the logarithm of the market capitalization of the company (“ln(Mktcap)”) (reflecting the greater propensity of larger firms to adopt majority voting);83 a variable for the percentage of shares held by institutional investors (“Insthold”); and a variable for whether a charter amendment is required to adopt majority voting (“CharterAmend”) (making such adoption harder). We note that our prior research indicated that company size is negatively associated with the percentage of “withhold” votes a nominee receives.84 To that extent, the size variable may also pick up some selection effect. The size variable may also reflect the potential pressure on the company to adopt majority voting because larger issuers may receive more media attention or greater governance pressure from institutional investors.85

In the Cox proportional hazards model, a coefficient estimate of less than one indicates that the variable is associated with a reduced likelihood of the adoption of majority voting, and a coefficient estimate of more than one indicates that the variable is associated with an increased likelihood of the adoption of majority voting. The z-statistics reported in Table 4 relate to whether the coefficient is different from one.

The results are reported in Table 4, Models 1 to 3. They indicate that having a prior record of ISS “withhold” recommendations is negatively associated with the adoption of majority voting. That is, a company whose nominees receive ISS “withhold” recommendations is less likely to adopt majority voting, as the selection hypothesis predicts. For example, Model 2 indicates that companies that had at least one ISS “withhold” recommendation in the past two years were, on average, 18.2 percent less likely to adopt majority voting than companies that had no ISS “withhold” recommendations, a decline that is statistically significant at the 5 percent level. In addition, in Models 2 and 3, the presence of a poison pill is associated with a significantly lower likelihood (at the 10 percent level) of adopting majority voting. We do not find, however, that low “withhold” votes for directors in prior years or the absence of a classified board (both evidence of shareholder responsiveness) correlate with an increased likelihood of a switch to majority voting. As predicted, larger companies and companies with a larger percentage of institutional investors are more likely to adopt majority voting. Companies with cumulative voting are less likely to do so.86

We examine two additional selection factors that are not directly related to corporate governance. First, we compare companies that are required to adopt majority voting through a charter amendment to those that can adopt it through a bylaw. As noted above, most states provide for plurality voting as the default rule but authorize individual firms to opt in to majority voting. In some states, majority voting must be provided for in the charter; in others (including Delaware), majority voting may be implemented through either a charter or bylaw amendment. Amending the corporate charter is more difficult than a bylaw amendment and typically requires both board approval and a shareholder vote.87 In Models 1 through 3, the coefficient on CharterAmend is less than one and is significant at either the 5 percent or 1 percent level. Unsurprisingly, we find that the mechanism of adoption affects the likelihood that firms will adopt majority voting; firms that can adopt majority voting only via a charter amendment are less likely to do so.correlate with an increased likelihood of a switch to majority voting. As predicted, larger companies and companies with a larger percentage of institutional investors are more likely to adopt majority voting. Companies with cumulative voting are less likely to do so.86

Second, we consider the extent to which the decision to adopt majority voting may be tied to firm performance. There are two possibilities. Better-performing firms may have more shareholder-oriented governance, in which case we might see a correlation between performance and adoption of an MVR. Alternatively, shareholders might seek greater accountability from the boards of firms that perform less well, so that a high return insulates a company from the pressure to adopt majority voting. Our findings are consistent with the latter explanation. For companies in the top 5 percent of abnormal stock price returns in the year before the annual meeting (Top5AbRet), the likelihood of adopting majority voting is only about half as high as it is for companies in the base category of comparison that are neither Top5AbRet nor Bot5AbRet (that is, those companies in the middle, with returns ranging from the 5th percentile up to the 95th percentile in the distribution of returns).

The analysis becomes particularly interesting when we differentiate between early and late adopters. We reestimated Models 1 through 3 of Table 4 for only the years from 2007 to 2009 and report these models as Models 4 through 6 of Table 4 (the early-adopter hazards models). We also reestimated Models 1 through 3 of Table 4 for those firms that were plurality voting firms in 2009 for the years from 2010 to 2012 and report these models as Models 7 through 9 of Table 4 (the late-adopter hazards models). As with the full sample, we find that the prior record of ISS “withhold” recommendations and the presence of a poison pill are negatively associated with the adoption of majority voting by early adopters. The effect is also economically significant. For example, in Model 5, the point estimates indicate that, during the early adoption period (2007 to 2009), having received an ISS “withhold” recommendation for any director in the last two years reduced the likelihood of adopting majority voting by 26.4 percent, and having a poison pill reduced the likelihood by 28.3 percent. By contrast, the variable for positive abnormal returns (which we interpret as a measure of either pressure to adopt majority voting or the board’s ability to resist such pressure) is insignificant.

For late adopters, by contrast, the variables that were significant for the full sample and that we took as indicators of shareholder responsiveness—the prior record of ISS “withhold” recommendations and the presence of a poison pill—are now insignificant. By contrast, the variable that may reflect reduced outside pressure to adopt majority voting or the ability to resist such pressure—positive abnormal returns—is significant, which is consistent with lower pressure or a higher ability to resist pressure making the adoption of majority voting less likely.88

In conclusion, we find some evidence consistent with early adopters of majority voting differing from those that retain a plurality standard: companies are more likely to adopt majority voting if they do not perceive their existing board members as being at risk of receiving an ISS “withhold” recommendation, or if they are generally more responsive to shareholder concerns (as proxied by the absence of a poison pill). We find no statistically significant evidence among early adopters that the ability to resist pressure is related to the adoption of majority voting. The evidence is consistent with the notion that early adopters adopt majority voting voluntarily because they believe that it reflects the principles of shareholder-friendly governance to which they already subscribe, and not due to outside pressure.

For late adopters, we find no statistically significant evidence of similar self-selection. In particular, we are unable to reject the hypothesis that late adopters do not differ from nonadopters in their prior electoral and ISS records. Late adopters, however, are less likely to have experienced abnormally positive stock price performance prior to adoption than nonadopters, which may have increased the outside pressure to make governance changes.

There is one caveat to our results. The lack of a statistically significant relationship for late adopters between the prior ISS record and the decision to switch to majority voting may be due to greater variance in the relationship. Despite this greater variance, it is possible that the average effect of the prior ISS record on the decision to switch to majority voting is similar for early and late adopters.89 The greater variance is nonetheless consistent with at least some late adopters adopting majority voting only semivoluntarily (that is, even if they have a poor prior ISS record) compared with early adopters.

A plausible interpretation of these results is that shareholder activists first pushed for the adoption of an MVR at firms where an MVR may have been largely costless (or at least low-cost) because these firms were already responsive to shareholders. As time went by and MVRs became accepted as a best practice, firms for whom an MVR was more costly—because they were less shareholder responsive—began to adopt it as well. Shareholder activists instead could have first targeted the least shareholder-responsive firms with their MVR campaigns as a way of improving the governance of the firms that, in their eyes, needed it most, ignoring the firms that were already responsive. This is inconsistent with our finding that the early adopters were most shareholder responsive, and thus does not seem to have been what happened.

2. The causation hypothesis: the effects of majority voting on subsequent electoral success.

One way to distinguish between selection and causation is to examine a particular firm both before and after the adoption of majority voting. To the extent that a firm that adopted an MVR had shareholder-friendly governance prior to adoption and maintained it throughout the measurement period, any changes in the actions of the firm and the level of voting support are not attributable to self-selection. If, however, the adoption of MVR changed director responsiveness to shareholders, increased the level of electioneering, or generated greater shareholder self-restraint, we would expect to see a reduction in “withhold” votes after the adoption of majority voting.

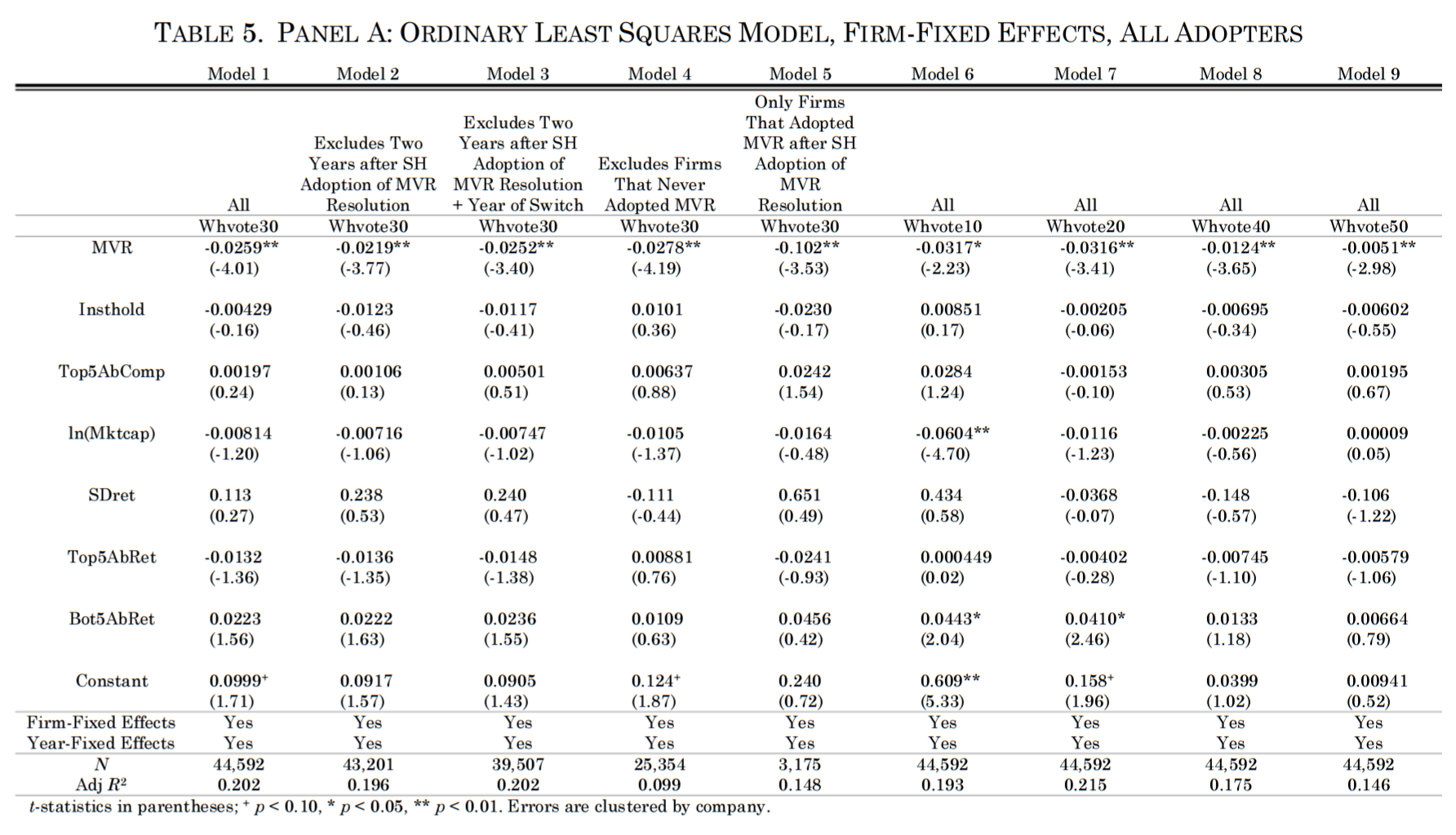

To test this possibility, we ran a set of ordinary least squares regressions on company-director-level data including firm-fixed effects. By including firm-fixed effects, we compare the record of each company after the adoption of majority voting to the firm’s own record prior to the adoption, after controlling for other factors. In particular, by including year-fixed effects, we also control for secular time trends. As dependent variables, we initially use an indicator variable for whether a specific director received a “withhold” vote of 30 percent or more (“Whvote30”).90 A 30 percent “withhold” vote is a sign of serious shareholder dissatisfaction.91 In robustness checks, we repeat our analysis with different thresholds.

Our key independent variable of interest is the variable “MVR,” which takes the value of one if the nominee is elected under an MVR and zero otherwise. The causation hypothesis predicts a negative coefficient for the MVR variable. We included as controls year-fixed effects and several variables that our prior research indicated may affect ISS recommendations or the percentage of “withhold” votes.92 These included a variable for the percentage of shares held by institutional investors (Insthold); whether the CEO of the company was in the top 5 percent of total excess compensation (“Top5AbComp”); the natural logarithm of the market capitalization of the company (ln(Mktcap)) (reflecting the greater propensity of larger firms to adopt majority voting); the standard deviation in the company’s stock return measured for the one-year period prior to the annual meeting (“SDret”); and two indicator variables for whether the firm was in the top 5 percent or bottom 5 percent of companies in our sample based on the abnormal holding period return for the one-year period prior to the annual meeting (Top5AbRet and Bot5AbRet).93

Model 1 includes observations for all years. Model 2 excludes observations for the two years following the adoption of a shareholder resolution calling for majority voting. Model 2 thus accounts for the possibility that shareholders may “punish” directors for a failure to implement majority voting—or “reward” them for implementing majority voting—following the adoption of such a resolution. Model 3 excludes, in addition, observations for the first year in which a company employed majority voting (regardless of whether there was a shareholder resolution), reasoning again that shareholders may “reward” these companies, resulting in an unusually low likelihood of a 30 percent “withhold” vote. Model 4 includes observations from only firms that eventually adopted majority voting. The results are reported in Panel A of Table 5.

The results of these regressions lend support to the hypothesis that adoption of majority voting induced some change in behavior. After a company adopts an MVR, the likelihood that a nominee of that company will receive a “withhold” vote in excess of 30 percent drops by 2 to 3 percentage points relative to when the company was under a PVR, a decline that is statistically significant.94 The results are robust to the exclusion of observations for the two years following the approval of a shareholder resolution calling for majority voting (Model 2), to the further exclusion of observations for the first year in which a company employed majority voting (Model 3), and to the exclusion of observations from firms that never adopted majority voting (Model 4).

Because the regressions employ firm-fixed effects, self-selection would not explain the results if the exogenous probability that a company nominee would attract a high “withhold” vote is stable over time for each company. However, the possibility exists that a firm suffered from an exogenous shock that decreased that probability and, due to that shock, also decided to adopt majority voting. To address this possibility, we ran a separate regression including observations from only firms that adopted majority voting after shareholders adopted a proposal calling for the institution of majority voting (Model 5). These firms adopted majority voting under significant pressure, rather than by choice. We again find a statistically significant decrease in the probability that a nominee of that company will receive a “withhold” vote in excess of 30 percent relative to when the company was under plurality voting.

We ran the regressions (with the full set of observations) using thresholds of 10 percent, 20 percent, 40 percent, and 50 percent, reported in Models 6 through 9 of Panel A of Table 5, and also obtained statistically significant results.95 We note, however, that the coefficients for MVR in the regressions using a 10 percent and a 20 percent cutoff are close to the coefficient for MVR in the regression using a 30 percent cutoff. In these regressions, the MVR coefficients represent the change in the likelihood of receiving a “withhold” vote above the threshold. Thus, for example, the likelihood of receiving a “withhold” vote above 30 percent, after controlling for firm-fixed effects and other factors, declines by 2.59 percentage points after a company adopts an MVR (as reported in Model 1). The likelihood of receiving a “withhold” vote above 10 percent declines by 3.17 percentage points after a company adopts an MVR (as reported in Model 6). The similarity in coefficients suggests that there is not a significant change in the likelihood of receiving a “withhold” vote between 10 percent and 30 percent and that the results in the regressions using these thresholds are driven by the reduced likelihood of a “withhold” vote in excess of 30 percent. We explore this further below.

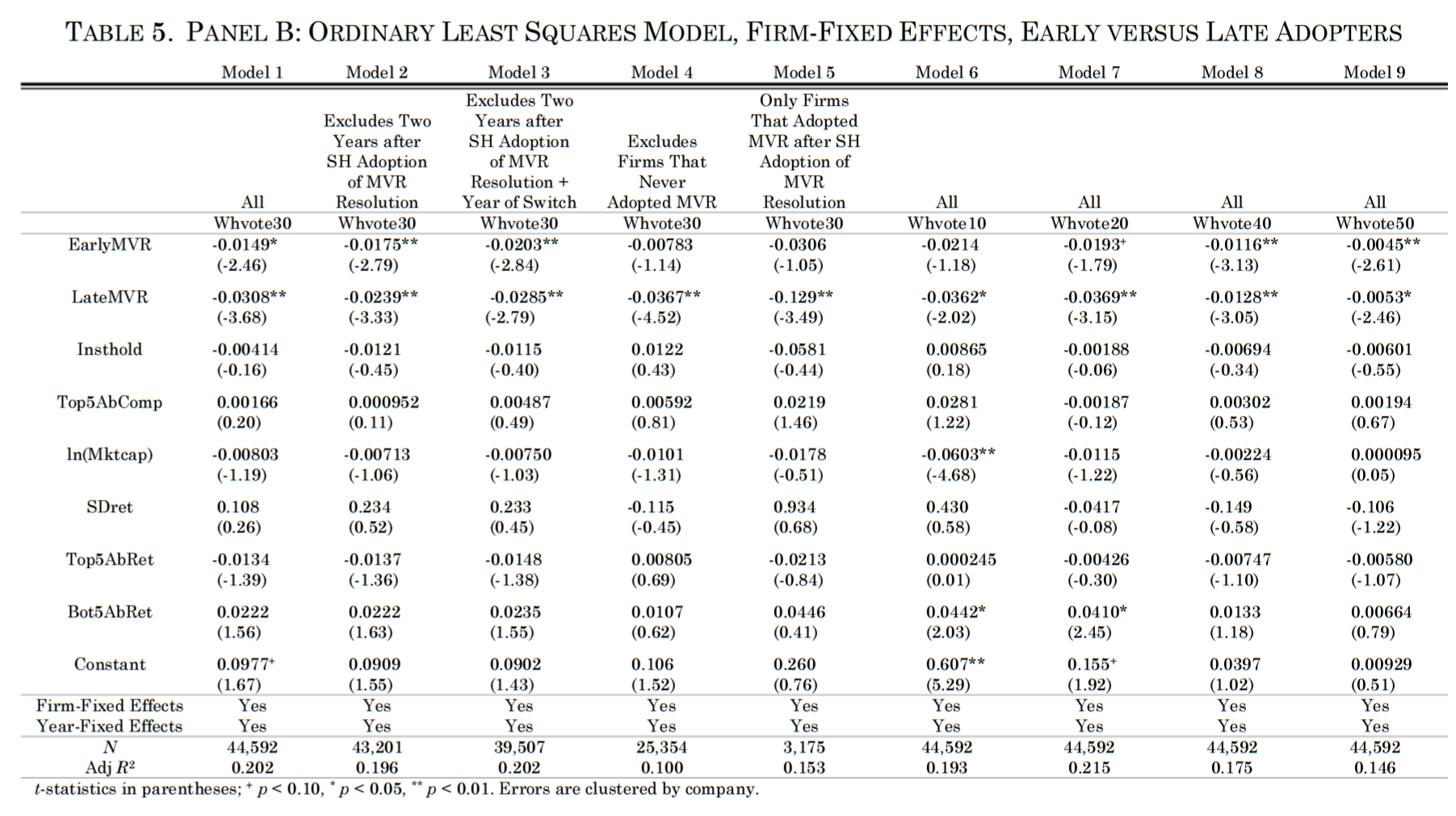

We next differentiated between early adopters and late adopters of majority voting for each model in Panel A by including separate dummy variables for each set of firms (“EarlyMVR” and “LateMVR”). We report the results in Panel B of Table 5. For each model in Panel B of Table 5, we include the same control variables as in Panel A of Table 5. The results for late adopters are statistically highly significant and of slightly higher magnitude than the results for adopters as a whole. The results for early adopters decline in magnitude relative to the results in Panel A, and in several specifications, are statistically insignificant. F-tests of the difference between EarlyMVR and LateMVR indicate that the difference is significant in Model 1 (p-value = 0.085), Model 4 (p-value = 0.001), and Model 5 (p-value = 0.038).

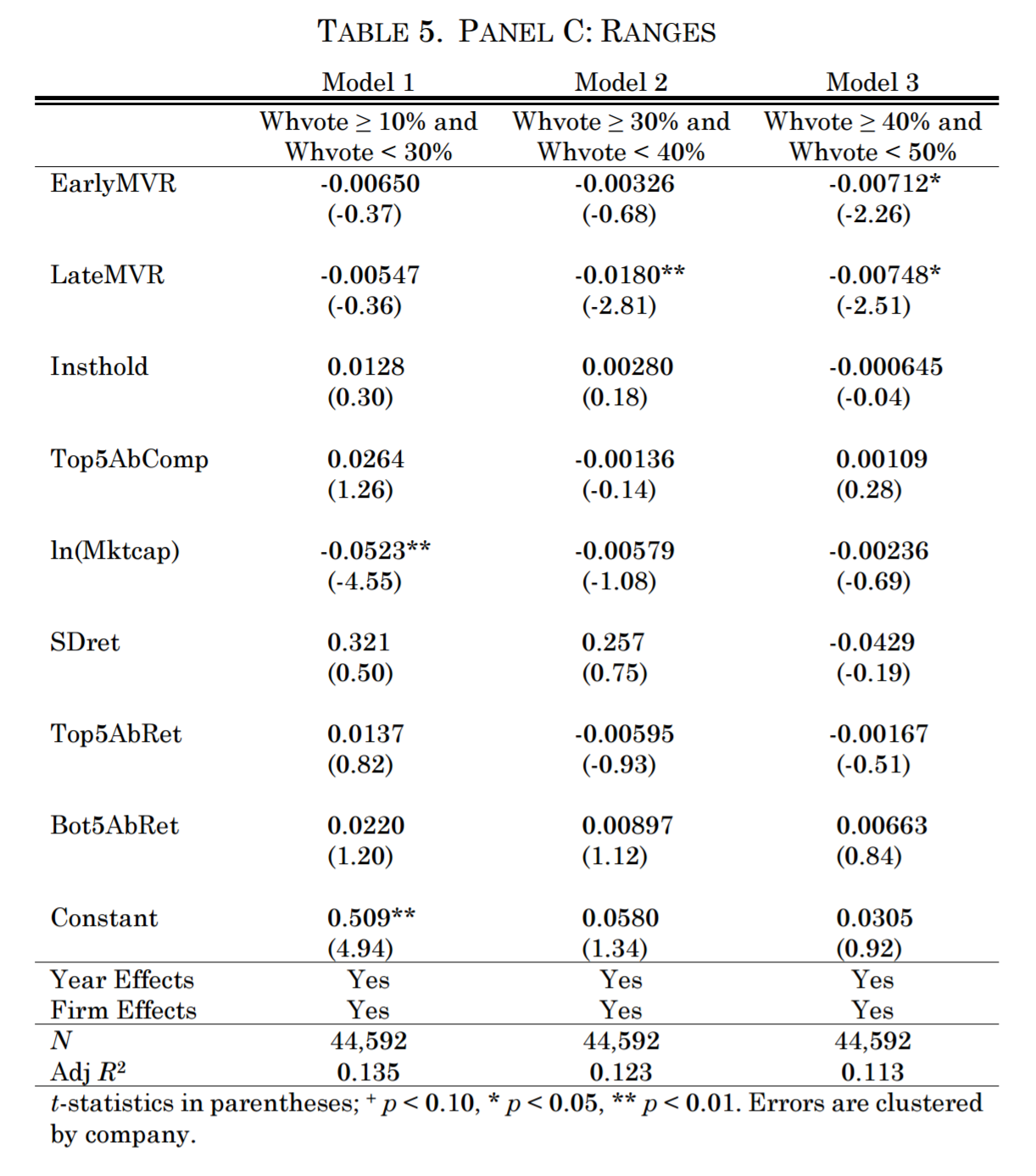

To target more specifically the threshold level at which an MVR reduces the probability of a “withhold” vote, we ran regressions in which the dependent variable was, respectively, whether a director received a “withhold” vote in the 10 to 30 percent range, in the 30 to 40 percent range, or in the 40 to 50 percent range. Panel C of Table 5 reports the results. For each model in Panel C of Table 5, we include the same control variables as in Panel A of Table 5.

|

|

The results for late adopters indicate a statistically significant and economically meaningful reduction in the probabilities for the 30 to 40 percent and the 40 to 50 percent ranges after the adoption of an MVR. For early adopters, only the reduction in probability for the 40 to 50 percent range was significant after the adoption of an MVR. For both sets of adopters, there was no significant effect on the probability of receiving a “withhold” vote in the 10 to 30 percent range after the adoption of an MVR. F-tests of the difference between EarlyMVR and LateMVR indicate that the difference is significant only in Model 2 for the 30 to 40 percent range (p-value = 0.050). In the 30 to 40 percent range, majority voting thus corresponds to a reduction in the probability of a “withhold” vote for late adopters relative both to nonadopters and to early adopters, and to no statistically significant reduction for early adopters.

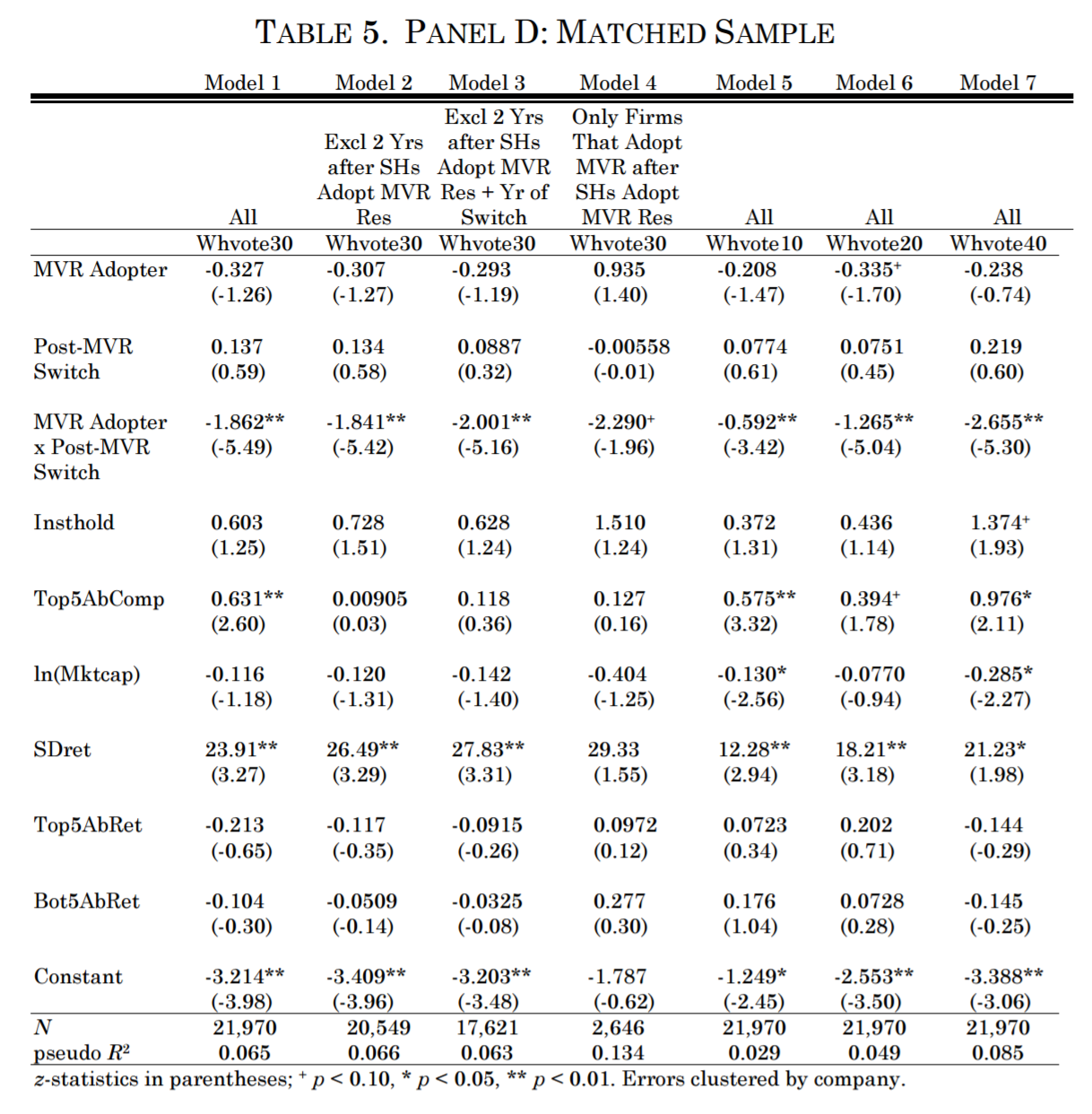

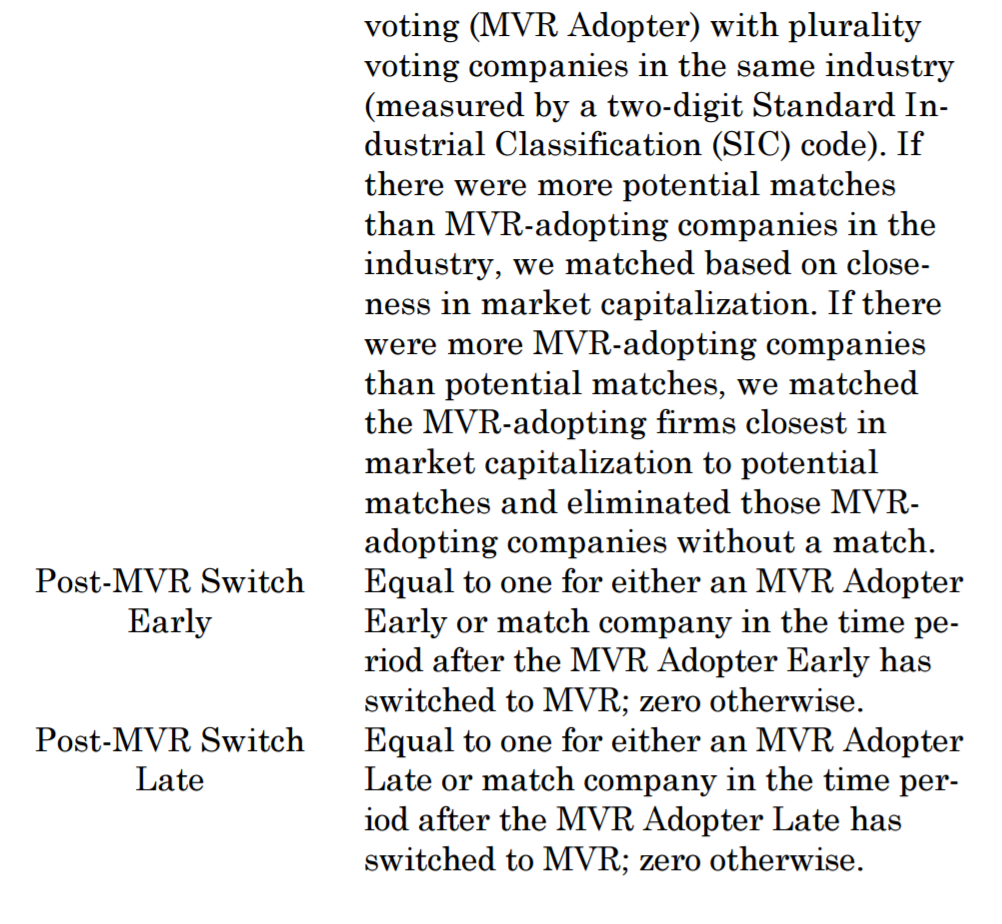

For further analysis, we matched firms that adopted majority voting with plurality voting firms in the same industry (measured by a two-digit Standard Industrial Classification (SIC) code). If there were more potential matches than MVR-adopting firms in the industry, we matched firms based on closeness in market capitalization. If there were more MVR-adopting firms than potential matches, we matched the MVR-adopting firms closest in market capitalization to potential matches and eliminated those MVR-adopting firms without a match.

We then looked at the difference in the likelihood of a high “withhold” vote between directors at the firm that adopted majority voting and directors at the matched firm. We looked at this difference before the adoption of MVR and at the difference in this difference after the adoption of MVR (“Post-MVR Switch” is assigned the value of one for the time period after the switch to MVR and zero for the time period before the switch). “MVR Adopter” measures the difference between firms that would eventually adopt an MVR and their matches both before and after the adoption of majority voting; Post-MVR Switch measures the difference during the post-adoption period for both firms that adopted MVR and their respective matches. Using a difference-in-differences model allows us to control for unobservable corporate governance differences between our matched firms. Panel D of Table 5 reports logit models of a director receiving a “withhold” vote of more than a specified threshold using MVR Adopter, Post-MVR Switch, and “MVR Adopter ´ Post-MVR Switch” as independent variables. MVR Adopter ´ Post-MVR Switch measures the difference-in-difference variable.96 Model 1 in Panel D of Table 5 includes observations for all years for director elections in MVR Adopter firms and their matching nonswitching firms. Model 2 excludes observations for the two years following the adoption of a shareholder resolution calling for majority voting. Model 3 excludes, in addition, observations for the first year in which a company employed majority voting (regardless of whether there was a shareholder resolution). Model 4 includes observations from only MVR Adopter firms that adopted majority voting after shareholders adopted a proposal calling for the institution of majority voting and their matching nonswitching firms. We also ran the regressions (with the full set of observations for MVR Adopter firms and their matching firms) using “withhold”-vote thresholds of above 10 percent, 20 percent, and 40 percent, reported in Models 5 through 7 in Panel D of Table 5.97

The results of this analysis show a statistically significant negative coefficient for the interaction variable MVR Adopter ´ Post-MVR Switch in each model in Panel D of Table 5—meaning that after the switch, firms that adopt majority voting are less likely to experience a high “withhold” vote relative to their matched firms than they were before they made the switch. In Model 1, for example, measured at the mean of all the independent variables, the difference-in-differences interaction variable corresponds to a 3.5 percentage point reduction in the probability of receiving a “withhold” vote above 30 percent.98 These results, for adopters as a whole, are consistent with the respective results in the firm-fixed effects test.

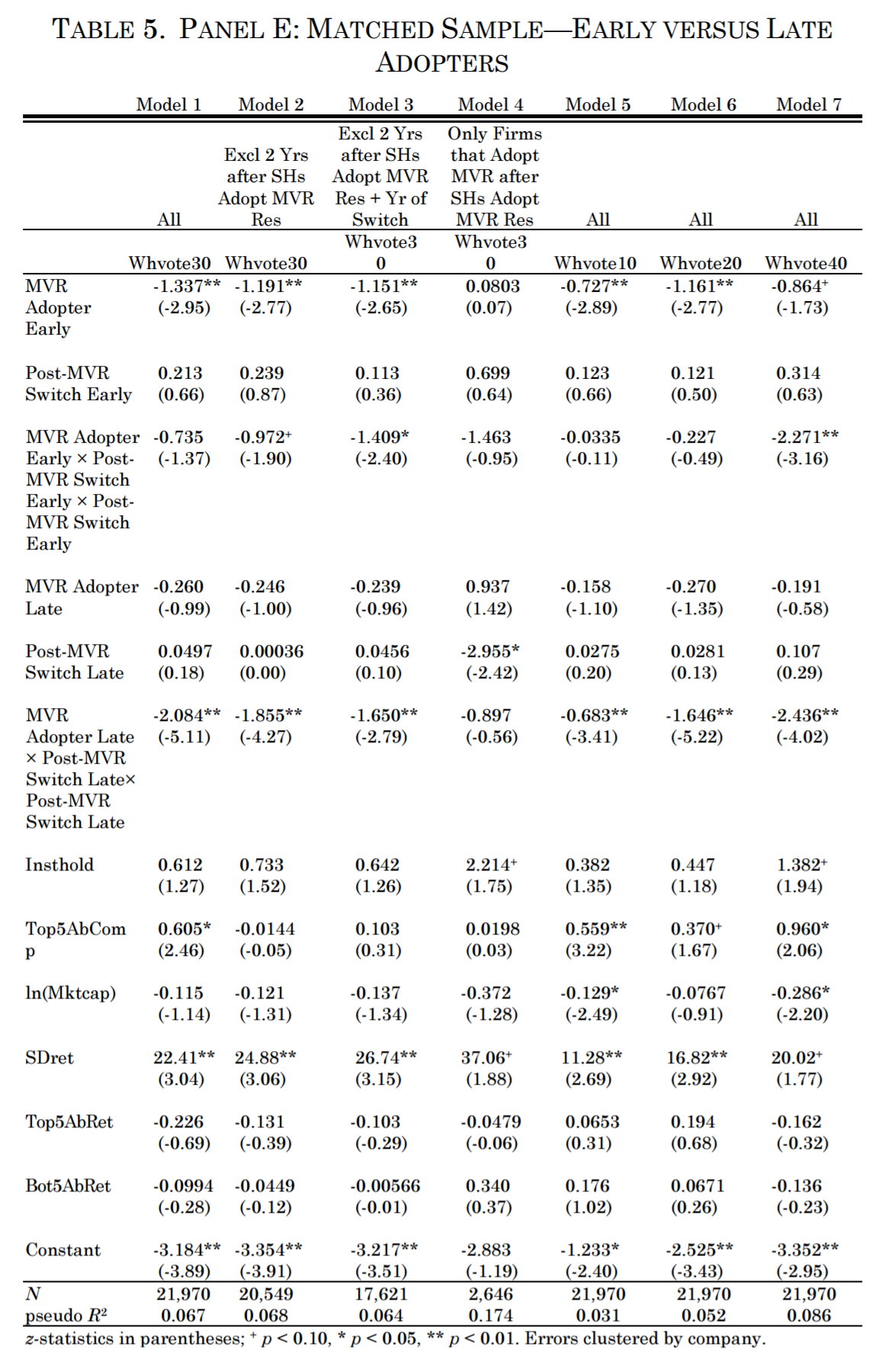

We next split the MVR Adopter and Post-MVR Switch variables from Panel D of Table 5 into separate variables for early adopters (“MVR Adopter Early” and “Post-MVR Switch Early”) and late adopters (“MVR Adopter Late” and “Post-MVR Switch Late”), and we included associated interaction terms. We report the results in Panel E of Table 5. When we segregate the sample by including separate dummy and interaction variables for early and late adopters, we find that the results for late adopters are robust. In Models 1 to 3 using the 30 percent threshold and in the regressions using the 10 percent, 20 percent, and 40 percent thresholds, the coefficient for the interaction variable is significant at the 1 percent level. The coefficient is insignificant only in Model 4, possibly due to the much smaller sample size. The coefficients for the interaction variables for late adopters are economically meaningful. Model 1, for example, measured at the mean of all the independent variables the difference-in-differences interaction variable for late adopters corresponds to a 2.8 percentage point reduction in the probability of receiving a “withhold” vote of above 30 percent.99

For early adopters, however, we find no significant results in Models 1 and 4 in Panel E of Table 5 and for thresholds of 10 percent (Model 5) and 20 percent (Model 6). We find weaker significant results in Models 2 and 3 (at the 10 percent and 5 percent level, respectively), and strong results in only the regression using a 40 percent threshold (Model 7). Note also that the coefficient for MVR Adopter Early is consistently and significantly negative (except in Model 4). This presents further evidence that early adopters had greater electoral success than other firms even before they adopted a majority vote rule—that is, evidence in favor of self-selection by early adopters. There is no equivalent evidence of self-selection by late adopters.

Overall, these results provide strong support for the proposition that the adoption of an MVR by late adopters reduced the likelihood of getting a “withhold” vote of 30 percent or above. We regard this result as most consistent with the deterrence or accountability hypothesis or some form of the electioneering hypothesis. While the shareholder-restraint hypothesis would also predict differential voting patterns, under that hypothesis the difference should be most pronounced around the 50 percent “withhold”-vote level at which the difference in voting rule transforms a message of dissatisfaction (under the plurality rule) into an actual effect on whether a nominee is elected (under the majority rule). For “withhold” votes of less than 50 percent, the message under both rules is similar. Thus, unless shareholders have great difficulty in predicting which votes will be close,100 shareholder restraint should not affect the likelihood of receiving a “withhold” vote in excess of 30 percent. Similarly, since companies obtain intermediate vote results during the solicitation process, they would almost certainly know whether any director were at risk of receiving a majority “withhold” vote.101 Different voting rules, therefore, should not affect electioneering efforts aimed at shareholders (such as calling individual shareholders who tend to support company nominees)102 in a way that results in different probabilities of receiving a 30 percent “withhold” vote.

Deterrence or accountability, however, may be a more plausible account for a different likelihood of receiving a “withhold” vote of more than 30 percent. At the time that directors decide whether to take an action that could result in a high “withhold” vote, directors may not yet know whether the resulting “withhold” vote will be around 30 percent or closer to 50 percent. To avoid the risk of a majority “withhold” vote, directors may thus refrain from taking the offensive action. This decision would also reduce the risk of a 30 percent “withhold” vote. This is especially true for actions that are likely to cause a large increase in “withhold” votes.103 Similarly, companies may engage in differential efforts to lobby ISS not to issue a “withhold” recommendation (a form of electioneering) because an ISS recommendation is correlated with a substantial percentage of votes and an ISS “withhold” recommendation is a virtual prerequisite to a majority “withhold” vote.104

Finally, an MVR may have more-subtle accountability effects. As some of us have argued elsewhere, the adoption of majority voting underlines the principle that shareholders are the bosses.105 This may lead to a change in board attitude and induce directors to adopt a more shareholder-centric view on other matters.106 Or, to the extent that a board was initially reluctant to adopt majority voting, the fact that proponents of majority voting eventually prevailed may be a show of strength that induces directors to offer less resistance to shareholder-rights advocates on other matters.107

By contrast, our results for early adopters provide support for the causation hypothesis only for levels of “withhold” votes in excess of 40 percent. Such an effect would be compatible with any of the three forms of causation hypotheses that we discussed: deterrence or accountability, electioneering, and shareholder restraint.

3. The deterrence or accountability hypothesis: the effect of the MVR on primary conduct.

To examine the deterrence hypothesis more directly, one could examine whether board actions, rather than electoral success, change after the adoption of majority voting. This question goes to the core of the claim that majority voting increases board accountability. An increase in shareholder support for directors after the switch to majority voting does not necessarily mean that the directors are behaving differently; voting results can alternatively be the result of electioneering by the issuer or restraint by shareholders under an MVR. The distinction between the deterrence hypothesis and the electioneering and shareholder-restraint hypotheses lies in whether majority voting affects primary board behavior (making the board less likely to take actions that generate shareholder opposition) or whether it affects the voting outcome given primary board behavior (reducing “withhold” votes due to electioneering or shareholder restraint). Evidence that primary board behavior changes after the adoption of majority voting would be evidence supporting the deterrence hypothesis, as distinguished from the electioneering and shareholder-restraint hypotheses. Evidence that the voting outcomes change after the adoption of majority voting even if there is no change in primary board behavior, in turn, would constitute evidence in favor of the electioneering or shareholder-restraint hypotheses, to the exclusion of the deterrence hypothesis.

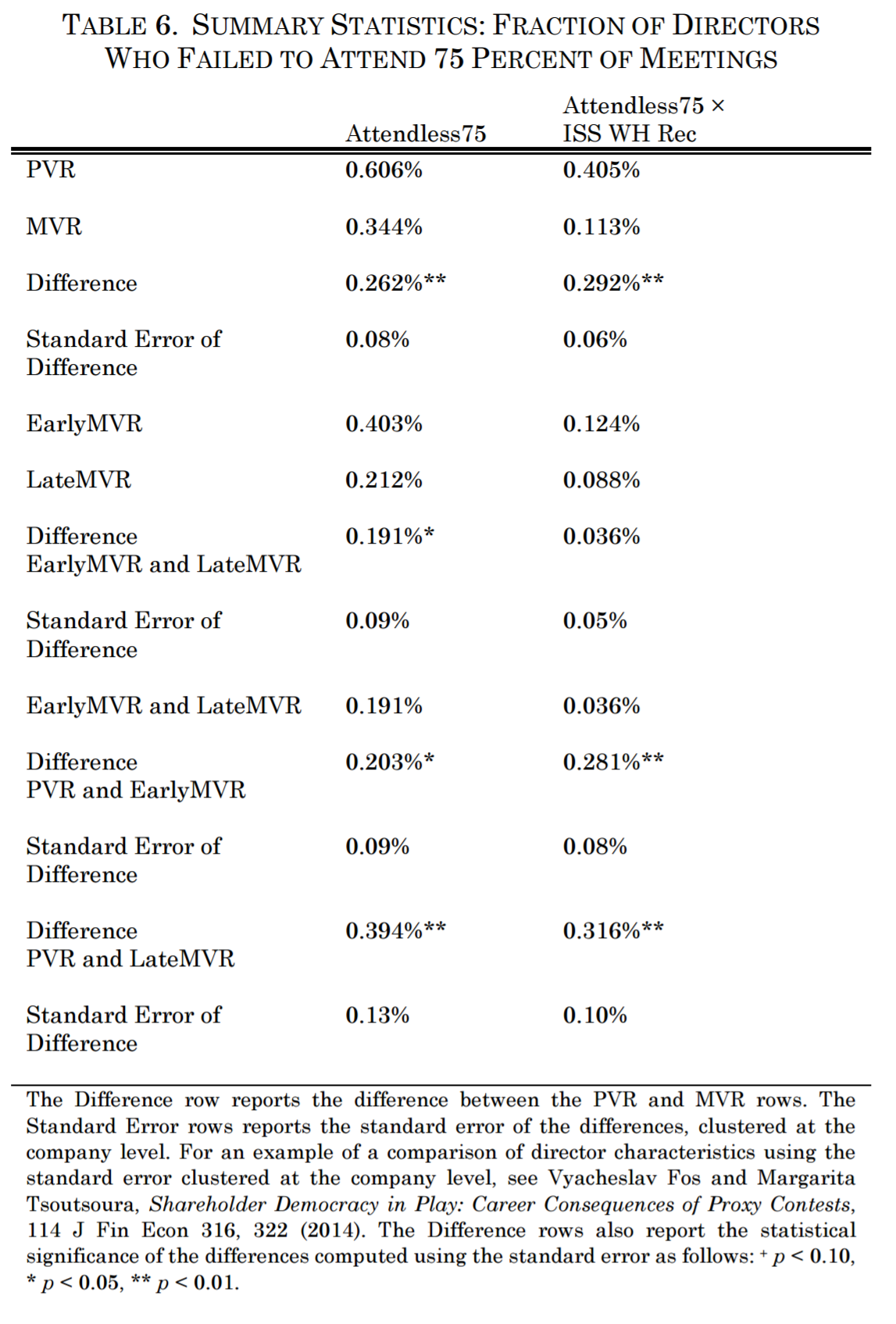

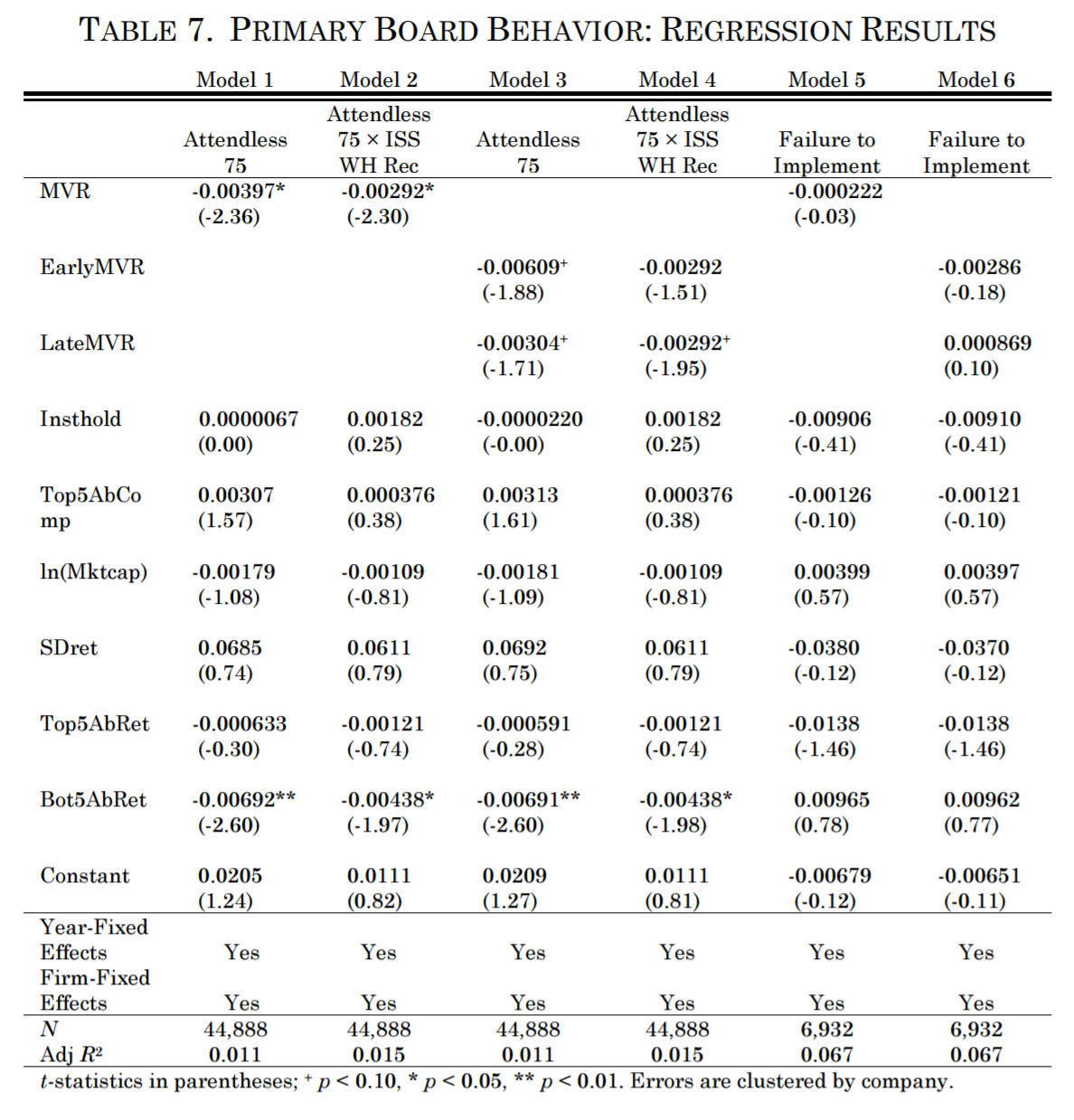

In prior research, three of us have identified two types of board behavior that are associated with a substantial increase in “withhold” votes: a director’s failure to attend at least 75 percent of the board or committee meetings (“Attendless75”) and a board’s failure to implement a shareholder proposal that had been adopted by shareholders (“Failure to Implement”).108 Attendless75, in particular, is strongly associated both with the likelihood of ISS issuing a “withhold” recommendation and with the expected “withhold” vote given an ISS “withhold” recommendation.109 If an MVR has any deterrent effect, it is especially likely to be reflected in Attendless75, given the substantial effect of such failure on “withhold” votes and the dichotomous nature of the variable.110

Both of these measures, however, also have problems. Companies can to some extent manipulate whether a director failed to attend at least 75 percent of the board or committee meetings. For example, if a director is just below that threshold, a company could schedule an additional committee meeting, if only a brief one, to enable the director to cross it. Similarly, many companies adopt, or promise to adopt, shareholder proposals before they come up for a vote, thereby inducing withdrawal of the proposal or rendering the proposal moot (and hence excludable from the proxy statement). The implementation rate of proposals that came to a vote and received majority support is thus a potentially biased measure of a company’s responsiveness to shareholder proposals. Moreover, to the extent that firms that employ an MVR and firms that employ a PVR differ in the degree of shareholder-oriented governance, as indicated by the earlier results, they may differ not just in their inclination to implement proposals but also in the likelihood that they will receive proposals that will be supported by a majority of shareholders. On the one hand, if their governance is more shareholder oriented, shareholders may perceive fewer problems that they want to address through proposals. On the other hand, if these firms are perceived to be more shareholder friendly, shareholders may make more proposals because they perceive a higher likelihood of adoption. Controlling for such endogeneity is thus a necessity.

In addition, Attendless75 may not be typical of other actions that induce a “withhold” vote. A failure to attend board meetings is one of the relatively few actions in which individual directors act contrary to the interest of the board as a whole. In a sense, they reflect director-board agency costs (in addition to director-shareholder agency costs). By contrast, most other actions that induce “withhold” votes—such as not implementing a shareholder proposal, approving abnormally high CEO compensation, or having business relations with the company—are approved by the board and are, at least arguably, in the best interest of the company (and thus reflect actual or perceived board-shareholder agency costs).

In Table 6, we provide summary statistics with respect to director attendance. The first column of Table 6 provides the percentage of directors who failed to attend the requisite percentage of meetings (Attendless75). The second column of Table 6 provides the percentage of directors who failed to attend the requisite percentage of meetings and also received an ISS “withhold” recommendation (“Attendless75 × ISS WH Rec”). The first column can be interpreted as a failure to attend for invalid as well as valid reasons (for example, temporary illness). The second column can be interpreted as a more precise measure of a failure to attend for invalid reasons, but it may also include the effect of ISS biases and of electioneering (that is, companies lobbying ISS not to issue a “withhold” recommendation).

To control for selection effects and possible time trends, we ran regressions using, respectively, Attendless75 and Attendless75 × ISS WH Rec as dependent variables, with independent variables including MVR, firm- and year-fixed effects, and the same additional controls as in Table 5.111 Our results, reported in Models 1 and 2 of Table 7, indicate that an MVR is associated with a statistically significant reduction in Attendless75 and Attendless75 × ISS WH Rec for adopters as a whole. These results present direct evidence that adoption of an MVR results in a reduced likelihood that directors will fail to attend at least 75 percent of the board meetings. We next test the effect of MVRs on early and late adopters, respectively (Models 3 and 4 of Table 7). The coefficients on LateMVR are negative and significant at the 10 percent level for both Attendless75 and Attendless75 × ISS WH Rec. For early adopters, the coefficient on EarlyMVR is negative and significant only for Attendless75 (Model 3 of Table 7). In both Models 3 and 4, F-tests of the differences between LateMVR and EarlyMVR are not significantly different from zero. We thus do not find evidence that the impact of adopting MVR on Attendless75 and Attendless75 × ISS WH Rec differs between early and late adopters of MVR.

We ran similar regressions using the failure to implement a shareholder proposal that received majority support as the dependent variable (Failure to Implement).112 Since the decision to implement a proposal is company-wide, these regressions were run on a company level. Results are reported in columns 5 and 6 of Table 7. The coefficients for whether the company has adopted majority voting are insignificant.113 We thus find no evidence of increased accountability with respect to this measure of shareholder friendliness.114

Both the deterrence and the selection hypotheses posit that nominees of majority voting companies behave differently than nominees of plurality voting companies (albeit for different reasons) and that this difference in behavior explains the differential vote patterns. But it is also possible that the same primary director behavior generates a different electoral outcome depending on the voting regime. Evidence of such a change in the voting outcome would constitute evidence in favor of electioneering and shareholder restraint.

To test for this possibility, we compiled a sample of director nominees who committed equivalent “offenses” against shareholder-friendly governance. We then calculated whether the probability of that nominee receiving a majority “withhold” vote115 differs depending on whether the nominee is elected under a PVR or an MVR. A higher likelihood for nominees subject to plurality voting would be consistent with electioneering by majority voting companies or restrained voting by shareholders of majority voting companies.

We identify the following five offenses:

- The nominee receiving an ISS “withhold” recommendation (ISS WH Rec);

- The nominee missing more than 25 percent of board and committee meetings (Attendless75);

- The nominee receiving an ISS “withhold” recommendation and missing more than 25 percent of board and committee meetings (Attendless75 ´ ISS WH Rec);

- The nominee being an incumbent director of a company that has failed to implement a shareholder proposal that has received majority support (Failure to Implement);

- The nominee receiving an ISS “withhold” recommendation and being an incumbent director of a company that has failed to implement a shareholder proposal that has received majority support (“Failure to Implement ´ ISS WH Rec”).

Note that some of these categories of offensive conduct include having received an ISS “withhold” recommendation. In these categories, a differential likelihood of receiving a majority “withhold” vote could reflect electioneering oriented toward shareholders. Any electioneering that takes the form of lobbying ISS not to issue a “withhold” recommendation may not be reflected in a differential likelihood of receiving a majority “withhold” vote.

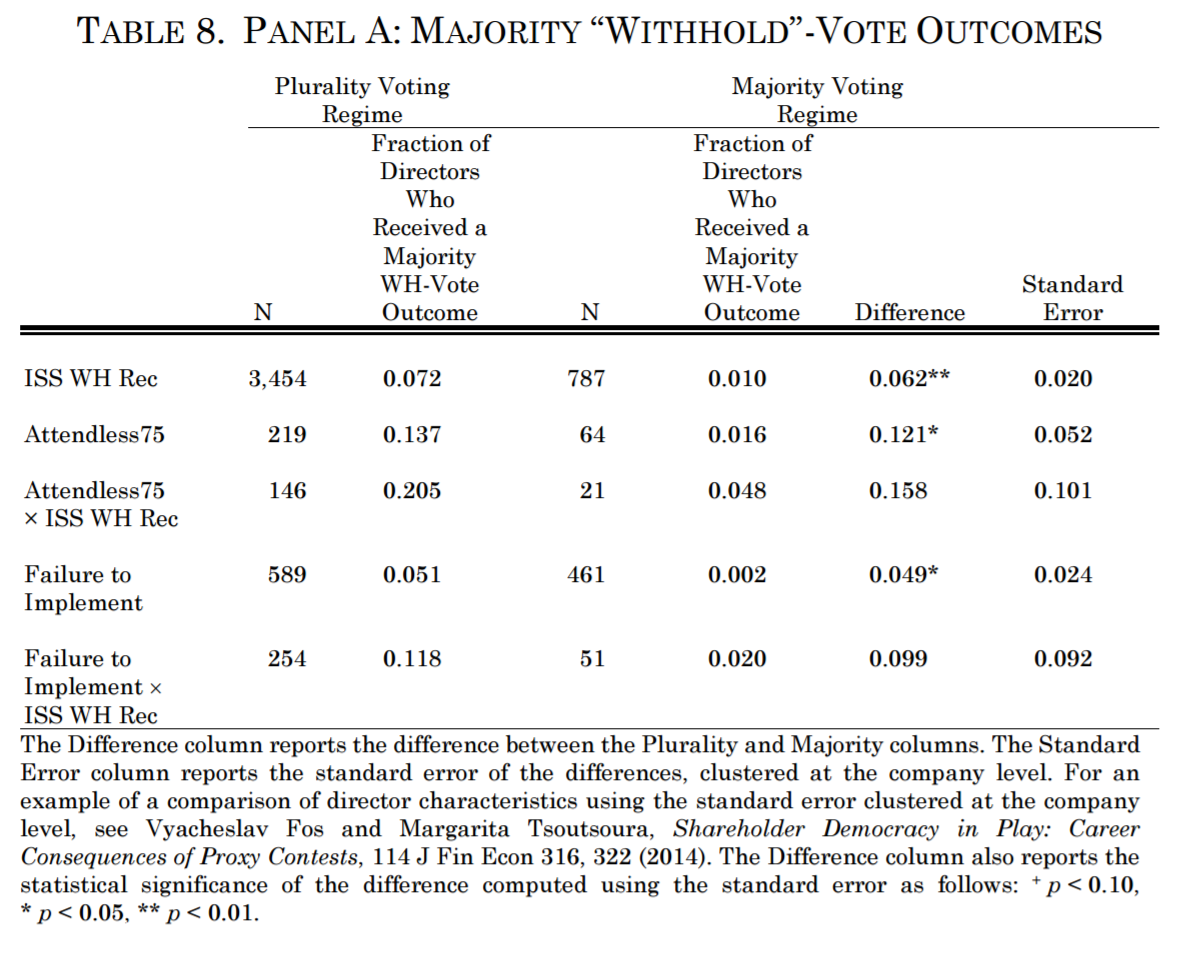

Panel A of Table 8 reports the summary statistics. In each category, the probability of receiving a majority “withhold” vote was substantially lower for nominees subject to an MVR than for nominees subject to a PVR. As Panel A shows, the likelihood of receiving a majority “withhold” vote given the primary behavior is significantly higher for plurality voting companies than for majority voting companies under each of the five measures. The differences, nonetheless, are significant only for ISS WH Rec, Attendless75, and Failure to Implement.

The results in Panel A, however, may be driven by selection effects. Different firms may have varying prior information on whether offensive conduct is likely to result in a majority “withhold” vote. For example, firms in which the board controls a high fraction of the votes are presumably less likely to receive a majority “withhold” vote than firms in which the board controls only a low fraction of votes. Firms that adopt an MVR may be those that are more sensitive to these priors than firms that choose to retain a PVR. Such MVR-adopting firms may generally be better able (whether under an MVR or a PVR) to assess when engaging in offensive conduct will not result in a majority “withhold” vote, and thus may engage in offensive conduct only in circumstances when it is unlikely to result in a majority “withhold” vote.

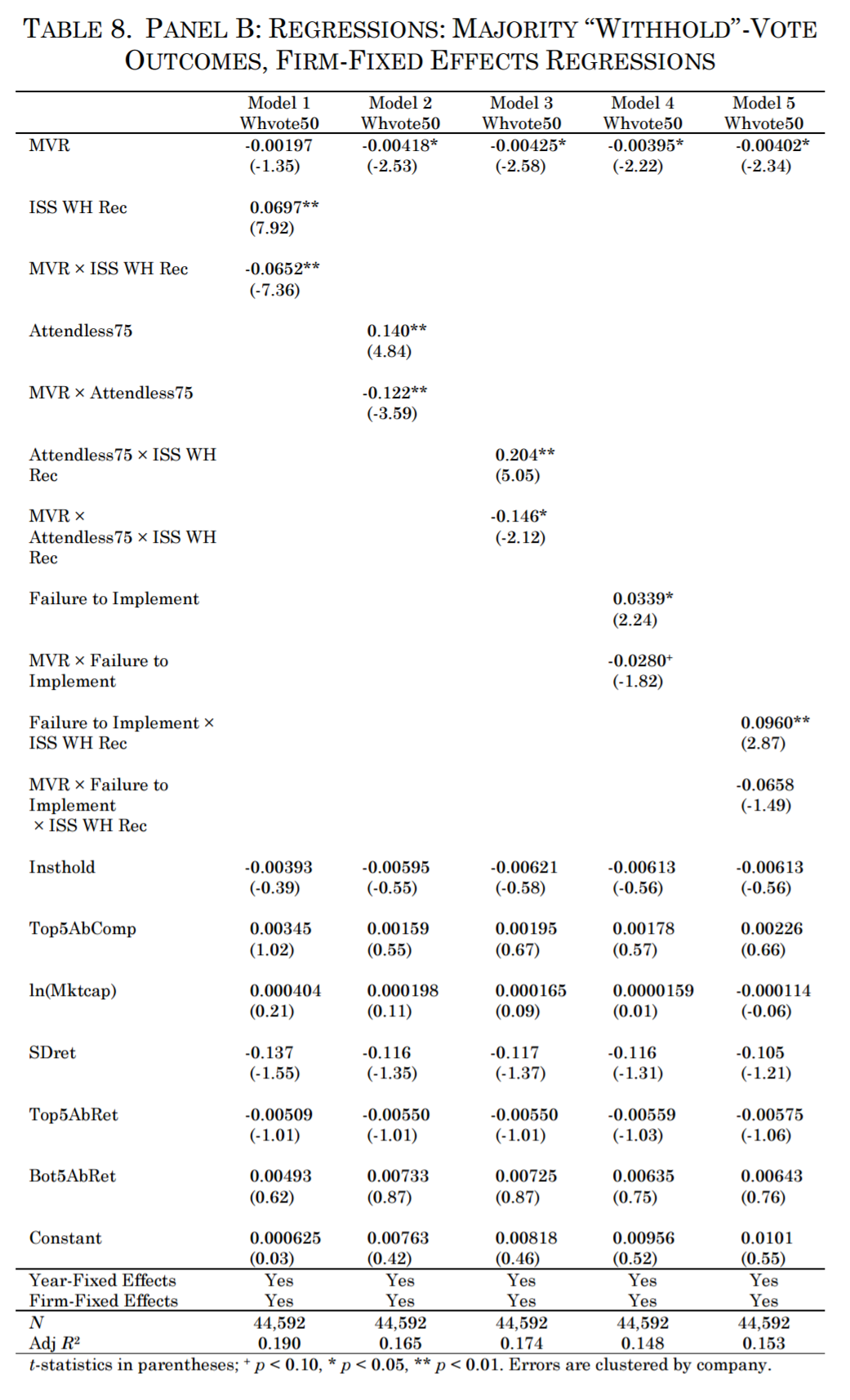

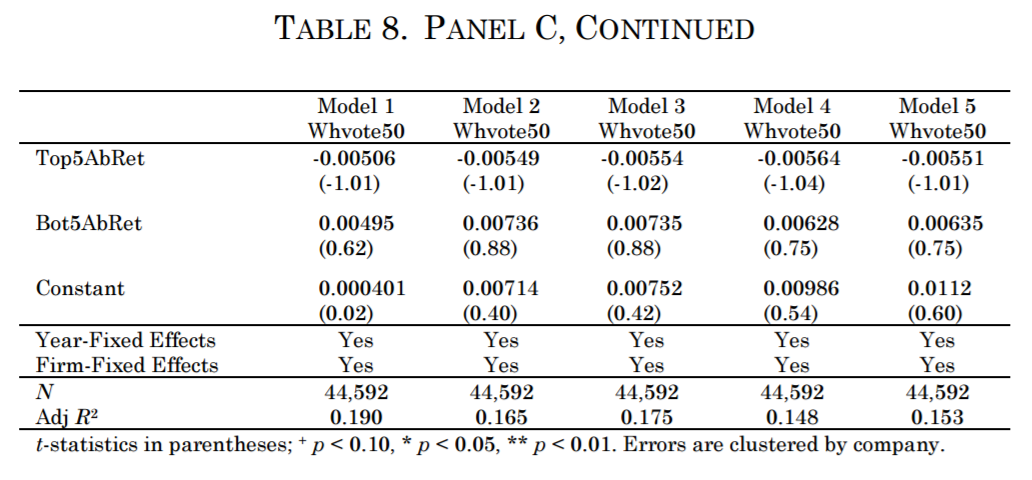

To address these selection effects, we ran firm-fixed-effects regressions. The dependent variable in these regressions is the likelihood of receiving a majority “withhold” vote. Because our a priori view is that electioneering or shareholder restraint will be most likely to take place when a vote otherwise may cross the 50 percent “withhold”-vote threshold, we focus on the likelihood of receiving a majority “withhold” vote to test the impact of electioneering or shareholder restraint. As independent variables, we include—in addition to firm-fixed effects—a dummy variable for an MVR, a dummy variable for one of the five “offenses,” an interaction of these dummy variables, and the same controls as in the models in Table 5.116 If, given the same offensive conduct, an MVR is associated with a reduced likelihood of a majority “withhold” vote, we expect a negative coefficient for the interaction dummy. We further predict a negative coefficient for the MVR dummy and a positive coefficient for the “offense”-conduct variable. These results are reported in Panel B of Table 8.117

|

|

Consistent with our predictions, the coefficient for MVR is significantly negative in four of the five regressions and the coefficient for the primary-conduct variable is significantly positive in each of the five regressions in Panel B of Table 8. In four regressions, the coefficient for the interaction variable between one of the offenses and MVR is significantly negative. Thus, even after controlling for endogeneity through firm-fixed effects, given similar conduct, MVR companies have a lower likelihood of receiving a majority “withhold” vote than do PVR companies.

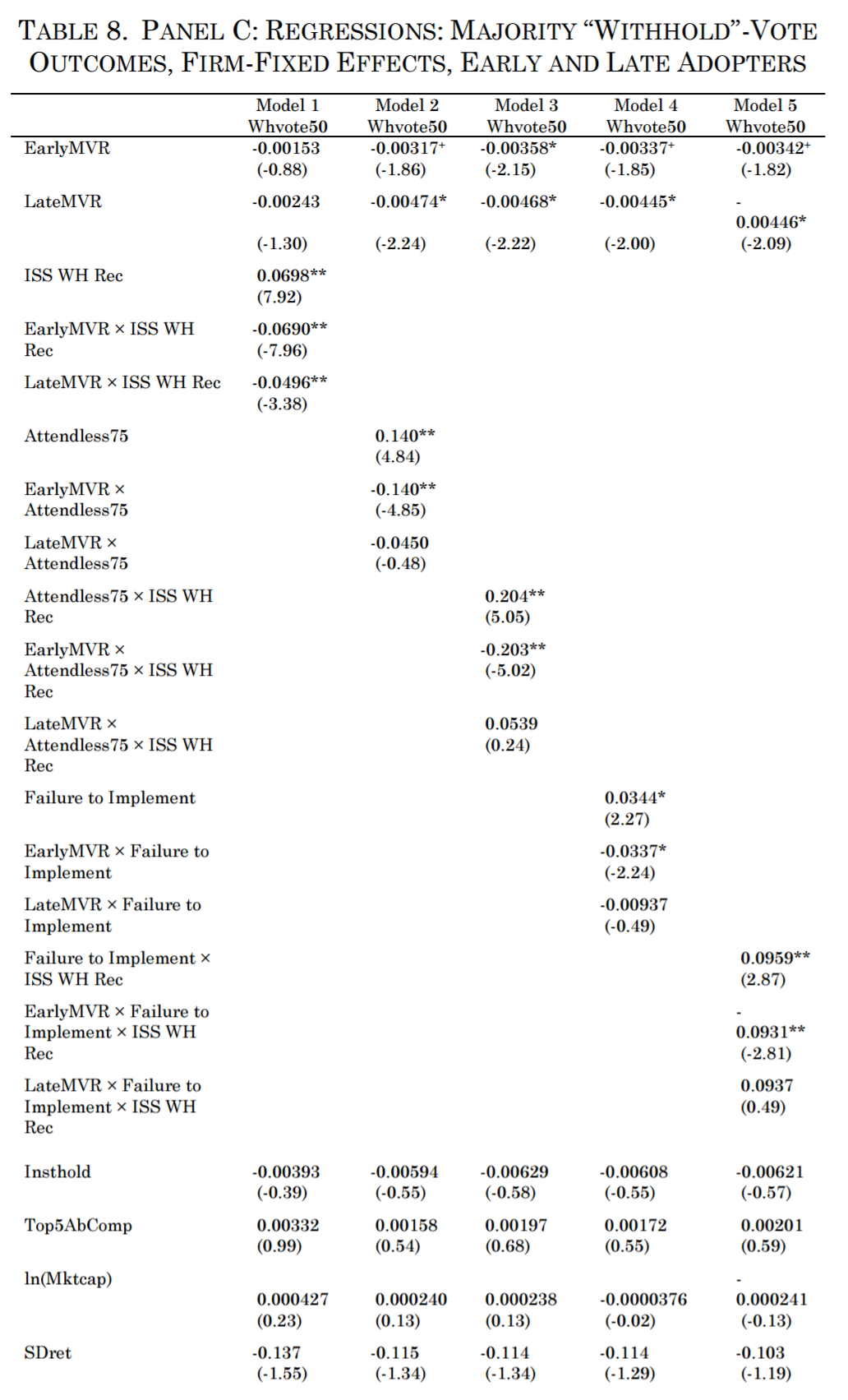

For each model in Panel B, we split the MVR variable into one for early adopters (EarlyMVR) and one for late adopters (LateMVR). We report the results in Panel C of Table 8. The interaction terms for the early adopters are statistically significant in all five regressions. Moreover, the sum of the “offense” variable and the interaction term between the “offense” variable and EarlyMVR is close to zero for each model, indicating that the negative effects of the offense on director voting are largely eliminated for the early adopters. Evidence for the electioneering or shareholder-restraint hypotheses therefore exists for the early adopters. For late adopters, however, only the interaction coefficient for the ISS “withhold” recommendation is significant.

The results in Table 8 could in principle reflect gradations in offensive conduct that are not captured by our variables. Thus, for example, the conduct of directors of plurality voting firms who receive ISS “withhold” recommendations may be systematically worse than the conduct of directors of majority voting firms who receive ISS “withhold” recommendations. While this may be plausible for some of our conduct measures, we think it is unlikely with respect to conduct defined as “failure to attend at least 75 percent of meetings and ISS ‘withhold’ recommendation” (Attendless75 × ISS WH Rec) and “failure to implement and ISS ‘withhold’ recommendation” (Failure to Implement × ISS WH Rec).

Moreover, the coefficient estimates for the interaction variable for early adopters are virtually identical to (and of the opposite sign as) the estimates for the respective-conduct variable. Thus, for example, in Model 3 of Panel C, the coefficient estimate for “failure to attend at least 75 percent of meetings and ISS ‘withhold’ recommendation” (Attendless75 × ISS WH Rec) is 0.204, indicating a 20.4 percentage point increase in the likelihood that a director at a plurality voting firm that engaged in such conduct would receive a majority “withhold” vote. The coefficient estimate for “failure to attend at least 75 percent of meetings and ISS ‘withhold’ recommendation” (Attendless75 × ISS WH Rec) interacted with early adopter (EarlyMVR) is -0.203, indicating a 20.3 percentage point decrease in the likelihood for a director at an early-adopting majority voting firm relative to a plurality voting firm. We are dubious that discrepancies of this magnitude can be explained by gradations in offensiveness within the group of directors who failed to attend at least 75 percent of meetings and also received an ISS “withhold” recommendation.

In sum, the results in Table 8 present strong evidence of electioneering or shareholder restraint for early adopters, although we are unable, on the basis of this test, to distinguish between the two hypotheses. By contrast, there is only weak evidence that electioneering or shareholder restraint affect the voting pattern for late adopters.

Director nominees at companies that adopt majority voting are far less likely to receive high levels of votes against them than are directors at plurality voting companies. The challenge is to explain why. Is it because firms likely to receive high levels of “withhold” votes are less likely to adopt majority voting, or does the adoption of majority voting cause a firm to become less likely to receive high levels of “withhold” votes? And if the latter, is the causal effect due to directors taking fewer actions likely to offend shareholder sensibilities, due to companies campaigning harder to reduce the level of “withhold” votes, or due to shareholders becoming more reluctant to withhold their vote because they anticipate that voting against a director nominee is not a mere protest vote but may have real consequences?

In our analysis, we obtain different results for early and late adopters of majority voting, in both the reasons for and the effects of adoption. For early adopters, we find evidence of selection effects: these companies had more electoral success and more shareholder-oriented governance before they adopted majority voting than firms that did not adopt majority voting. We conclude that early adopters largely adopted majority voting voluntarily. By contrast, we do not find statistically significant evidence that late adopters differ from nonadopters.

For both early and late adopters, we find statistically significant evidence that the adoption of majority voting affected voting results subsequent to the switch to majority voting. The reasons for this effect may differ, however, for these two sets of firms. For late adopters, we conclude that adoption of majority voting led to more shareholder-friendly governance, either because of the heightened threat that a majority “withhold” vote would lead to ouster from the board or because the adoption of majority voting made boards more sensitive to shareholder concerns. We find little evidence that late adopters enhanced their electoral fortunes through electioneering or that they benefited from shareholders’ restraint.

For early adopters, by contrast, we find evidence consistent with either electioneering or shareholder restraint. Outside of the specific context of inducing directors to attend sufficient board and committee meetings to meet the 75 percent attendance threshold, however, it is unclear whether adoption of majority voting had much effect on director behavior for early adopters.

The difference in our results for early and late adopters has broader lessons for understanding the spread of corporate governance innovations. In principle, there are two plausible strategies that shareholders can use to select targets for governance reform. The first is to target companies that are most in need of governance reform, at which the reform will have the most impact and the company is arguably least able to resist. The second strategy is to target companies that already have the most shareholder-friendly governance, at which, although the reform will have the least impact, the company is most amenable to adopting the innovation (either because it is committed to shareholder-friendly governance or because it realizes that the innovation will make little difference). Once the innovation has become established at shareholder-friendly companies, shareholders might then proceed to target those companies that are most in need of the reform, at a time when these companies are less able to resist because the reform is less novel or has even become a governance norm. At least for the introduction of majority voting, one of the most widely adopted innovations over the last decade, the results suggest that shareholders may have pursued the second strategy and been highly successful.

The implications of this study may apply to the spread of other governance reforms. Current innovations, for example, include proxy access and empowering a percentage of shareholders to call a special meeting.118 As with majority voting, institutional investors have urged issuers to adopt these changes. It will be interesting to examine which of the strategies investors pursue to induce companies to adopt these changes and whether that strategy succeeds.

That governance innovations can spread in different ways has important implications for the conduct and interpretation of empirical studies of corporate governance. First, this study highlights the importance of segregating early and late adopters of the innovations, because the reasons for and the effects of adoption may differ systematically between these groups. Second, one needs to be cautious in extrapolating results from studies conducted relatively early in the adoption process. Depending on the strategy employed by shareholders seeking governance reform, the effect of an innovation may be significantly higher or lower for early adopters than for subsequent adopters.

- 19See note 1.

- 20See 8 Del Code Ann § 216. Very few states provide for a non-PVR default. See Ala Code Ann § 10A-2-7.28; Alaska Stat Ann § 10.06.415; 805 ILCS 5/7.60; Mo Ann Stat § 351.265 (providing that an MVR is the default for corporations that do not have cumulative voting); ND Cent Code § 10-35-09 (same); NM Stat Ann § 53-11-32; SD Cod Laws §§ 47-1A-725, -728. See also Mary Siegel, The Holes in Majority Voting, 2011 Colum Bus L Rev 364, 369 & n 18 (“Only five states, however, provide majority voting as the default rule.”).

- 21See Harris, Missing in Activism, 2010 Colum Bus L Rev at 120–21 (cited in note 3).

- 22As officers and directors virtually always hold at least some stock, the election of the issuer’s nominees in an uncontested election with a PVR is a virtual certainty. See, for example, Trends in Board of Director Compensation (Harvard Law School Forum on Corporate Governance and Financial Regulation, Apr 13, 2015), archived at http://perma.cc/M5VZ-BLRL (noting that “companies typically provide [ ] equity awards and require minimum stock ownership” of directors).

- 23See Joann S. Lublin, Directors Lose Elections, but Not Seats (Wall St J, Sept 28, 2009), online at http://www.wsj.com/articles/SB125409320578444429 (visited July 9, 2016) (Perma archive unavailable) (reporting that ninety-three board members at fifty issuers received less than a majority of votes cast during 2009, but that none lost a board seat because they all served at issuers with plurality voting).

- 24See generally Joseph A. Grundfest, Just Vote No: A Minimalist Strategy for Dealing with Barbarians inside the Gates, 45 Stan L Rev 857 (1993).

- 25See Diane Del Guercio, Laura Seery, and Tracie Woidtke, Do Boards Pay Attention When Institutional Investor Activists “Just Vote No”?, 90 J Fin Econ 84, 85 (2008) (studying 112 publicly announced “just vote no” campaigns sponsored by institutional investors between 1990 and 2003).

- 26See Bruce Orwall, Calpers to Withhold Voting for Eisner (Wall St J, Feb 26, 2004), online at http://www.wsj.com/articles/SB107774511301139206 (visited Dec 5, 2015) (Perma archive unavailable).

- 27See Stephen Choi, Jill Fisch, and Marcel Kahan, The Power of Proxy Advisors: Myth or Reality?, 59 Emory L J 869, 870–71 (2010) (describing the services provided by proxy advisors).

- 28See Stephen Choi, Jill Fisch, and Marcel Kahan, Who Calls the Shots? How Mutual Funds Vote on Director Elections, 3 Harv Bus L Rev 35, 39 (2013). For further analysis on the role and influence of proxy advisors, see generally Yonca Ertimur, Fabrizio Ferri, and David Oesch, Shareholder Votes and Proxy Advisors: Evidence from Say on Pay, 51 J Accounting Rsrch 951 (2013).